Price wars and survival: China’s NEV sector enters its toughest phase

July 01, 2026

After years of rapid growth, China’s NEV industry faces a brutal shakeout

China’s NEV industry has grown exponentially, but with brutal price wars and pressure to survive, it is facing its toughest challenge yet

Chinese new energy vehicles (NEV) now hold a 61% share of the global market, but an ongoing domestic price war is the crucible in which the future of the industry is being forged, as larger champions—boosted by heavy state subsidies—are emerging to dominate the sector, while numerous smaller firms are unable to make the cut.

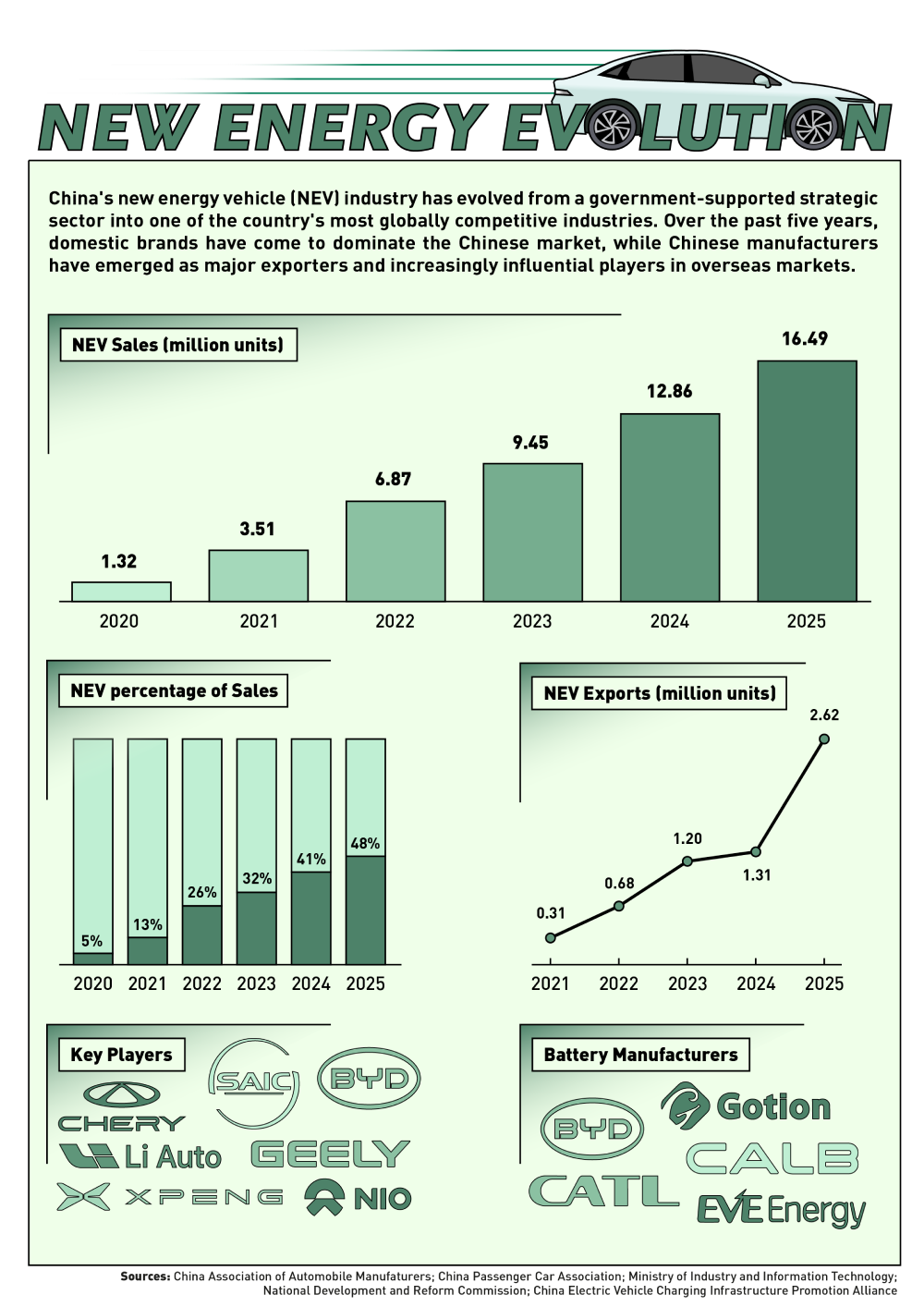

NEV production in China surged by nearly 30% last year, as output of traditional combustion-engine cars continued declining. EV sales exceeded 60% for the first time in April, with gas guzzlers now below 40%.

According to industry data, China produced approximately 12.9 million NEVs in 2025 and exported more than 2 million vehicles. Yet despite record output, profitability remains elusive. The auto sector’s average profit margin fell to just 3.2% in the first quarter, while many EV startups continue to report annual losses as they spend heavily on research, autonomous driving systems and overseas expansion.

“The market is now crowded, price-sensitive and competition increasingly defined by cost control, battery performance and smart-driving features,” says David Zhang, an analyst at Trivium China. He added that the three years of relentless price war have driven the Chinese EV market from a high growth “adoption” phase into a much more brutal consolidation phase characterized by technological competition, consolidation and survival pressure.

The threats not only compound challenges to domestic players, but also foreign automakers trying to survive in an already cutthroat domestic market–in April, the penetration rate of domestic brand NEVs reached a record high of 80.1%.

“With domestic demand under pressure, a persistent price war and a saturated market of new models, the battle for automakers is no longer just about sales volume,” says Liu Qiujun, a stock analyst at a Shenzhen-based capital management firm.

“It’s about whether they can maintain profit margins while slashing prices, sustain a pipeline of appealing products and build a genuine competitive moat in both intelligence and global expansion.”

A helping hand from the state

China’s EV ascent was forged by a potent cocktail of state subsidies and industrial policy designed to cultivate global champions. From aggressive consumer incentives and subsidies to automakers, government-funded infrastructure to a regulatory environment that favored domestic players, China methodically engineered the world’s largest, most sophisticated EV ecosystem.

This didn’t just drive demand; it acted as a force multiplier for producers to scale with unprecedented speed, Zhang says.

Companies like BYD scaled rapidly by localizing supply chains, particularly in batteries and critical components. The pressure was so immense that even global incumbents—Tesla included—were forced to localize production just to stay relevant in the world’s most demanding consumer market.

Over time, China evolved into the automotive industry’s “hard mode.” Product life cycles compressed to a blink-of-an-eye pace, domestic consumers embraced new technologies at a rate far outpacing their Western counterparts, and local governments turned charging infrastructure and urban policies into the bedrock of a new, high-velocity competitive landscape.

While government subsidies played a critical role in jump-starting China’s EV industry, they were only one part of a broader ecosystem that enabled the sector’s rapid expansion, says Liu.

China’s EV market was ultimately driven by a combination of purchase tax exemptions, license-plate incentives in major cities, charging infrastructure investment, falling battery costs and the improving competitiveness of domestic brands,” she says.

That environment rewarded companies able to move quickly on pricing, software and manufacturing scale. It also intensified competitive pressure to levels rarely seen elsewhere.

“Ironically, this ecosystem also contributed to the current overcapacity problem by encouraging too many localities and companies to pile into the sector. Beijing is now recalibrating support to stop subsidizing sheer volume and start rewarding quality and consolidation,” Trivium’s Zhang says.

The Cost of Rapid Growth

The explosive growth that helped propel China to the forefront of the global EV industry has come at the expense of profitability. Despite rising sales volumes, industry margins have fallen to historic lows, exposing the financial strain beneath the sector’s headline success.

More than 100 EV brands currently compete in China, according to industry estimates, but analysts increasingly expect consolidation to leave perhaps a dozen major survivors over the longer term. Several once-prominent startups, including WM Motor and HiPhi, have already encountered severe financial difficulties or ceased operations altogether.

Much of that pressure stems from a three-year price war that reshaped the competitive landscape. Often seen as triggered by Tesla’s aggressive price cuts and amplified by domestic automakers such as BYD, which promoted EVs as cheaper alternatives to gasoline-powered vehicles, manufacturers repeatedly slashed prices in an effort to gain market share.

While consumers benefited from lower costs and the EV market expanded rapidly, the strategy eroded profitability across the sector, intensified competition and compounded pressure on weaker players, says Wei Hongxu, a researcher with Anbound, a Beijing-headquartered independent think tank.

“The price war is unlikely to be sustainable much longer,” he says.

“It erodes automakers’ ability to invest in research and development and weakens long-term product competitiveness,” Wei says. “As market growth slows, further price cuts are no longer creating significant new demand but simply intensifying competition among manufacturers. If this continues, it will ultimately hurt both consumers and the industry,” he says.

Regulators have increasingly expressed concern over ‘disorderly competition.’ Earlier this year, China’s industry ministry and market regulators convened automakers and urged companies to resist excessive price wars and promote ‘fair competition.”

Signs are now emerging that the industry may be reaching the limits of price-driven growth. Since the second quarter, more than a dozen EV brands, including NIO, XPeng and Zeekr, have raised prices or reduced discounts. Xiaomi increased prices on its SU7 sedan, while BYD raised prices on certain autonomous driving packages.

The shift reflects mounting cost pressure. Industry analysts say rising lithium carbonate prices and higher semiconductor costs have increased per-vehicle production expenses by thousands of yuan, making sustained discounting increasingly unsustainable.

Consumer attitudes are also changing. Frequent price cuts created expectations that waiting would lead to cheaper cars, encouraging buyers to delay purchases and reinforcing a ‘wait-and-see’ mentality.

Increasingly, however, consumers appear to be growing weary of endless discount cycles. According to McKinsey’s latest China consumer survey, 22.2% of consumers who purchased a vehicle in the past year held a negative view of the price war, compared with 16.5% who viewed it positively.

As a result, buyers are becoming more willing to pay for technology upgrades, intelligent driving systems, software capabilities, safety features and stronger brand differentiation rather than simply choosing the cheapest option.

That transition favors larger players with stronger balance sheets and deeper technological capabilities.

Leading domestic firms such as BYD are consolidating their position through supply chain control, manufacturing scale and cost efficiency. China’s battery ecosystem has also become increasingly self-sufficient, strengthening the competitiveness of local automakers.

At the same time, many smaller EV startups are facing severe financial pressure. High research and development costs, shrinking margins and slower funding flows are accelerating industry attrition. Companies unable to achieve scale are increasingly vulnerable in a market where price competition alone is no longer enough.

Industry experts say the shakeout is not surprising given the capital-intensive nature of the automotive sector.

“The auto industry is both capital-intensive and technology-intensive, which creates inherently high barriers to entry. That is one of the main reasons many young EV companies struggle to survive,” Wei says.

While consolidation is expected to accelerate, some do not expect China’s EV market to evolve into a winner-takes-all landscape.

BYD remains the clear market leader, with significant advantages in scale, cost control and supply-chain integration, Liu points out.

“But I do not believe China’s EV market will ultimately be dominated by a single company,” Liu says.

“The market is large and highly segmented. Companies including Geely, Changan, Chery, Leapmotor, Xiaomi, Li Auto, NIO, XPeng and Huawei-backed brands are each targeting different consumer groups and price points,” says Liu. “Some compete on affordability, others on intelligent driving, family-oriented features, brand positioning or ecosystem integration.

“What is more likely is greater concentration among leading players, while competition within that group remains intense.”

More hurdles for foreign players

Foreign automakers face particularly acute challenges. Traditional players such as Volkswagen and BMW remain heavily exposed to declining combustion-engine demand in China, while many of their EV offerings lag domestic rivals on software features, pricing and speed of innovation.

Joint venture structures, once critical to succeeding in China, can now slow decision-making and product adaptation. Domestic competitors are able to iterate faster, launch new models more frequently and tailor products more closely to Chinese consumer preferences.

As a result, many foreign automakers are being forced to rethink traditional partnership models and deepen cooperation with Chinese EV and technology companies, observers say.

The formula for success now is “in China, for China, at China speed,” meaning China-specific models and faster product cycles, local software development and supply chains, Trivium’s Zhang points out.

“They need to realize that competing in China now requires more than bringing a global platform into the market and adapting it slightly,” says Zhang. “A successful product must be designed around Chinese consumer expectations from the start.

“The hard truth is the foreign-brand premium is gone. Survival means matching local cost and technology, and accepting a smaller, profitable position instead of chasing share.”

To remain competitive, foreign automakers are increasingly localizing research and development, partnering with Chinese technology firms and accelerating software integration. Volkswagen, for example, has expanded cooperation with Chinese EV startups and autonomous driving suppliers to better adapt to local demand.

China’s EV market is therefore entering a new stage–one defined less by explosive expansion and more by consolidation.

The New Order

The industry’s next phase is unlikely to be defined by sales growth alone. As China’s EV market matures, competition is increasingly shifting from pricing to technology, operational efficiency and global expansion.

Consolidation is expected to accelerate, with weaker players struggling to survive in an environment of shrinking margins and rising investment requirements. The winners are likely to be companies that can combine manufacturing scale, supply-chain control and technological innovation while maintaining financial discipline.

For foreign automakers, the challenge is becoming increasingly structural rather than cyclical. China is no longer simply the world’s largest auto market–it is also one of its most technologically demanding, favoring companies capable of rapid iteration, deep localization and seamless integration with the country’s broader industrial ecosystem.

The companies that ultimately emerge as industry leaders may not necessarily be those that cut prices the most aggressively, says Liu.

“The long-term winners will be companies with scale, strong cost control, advanced intelligent-driving capabilities and highly efficient supply chains,” she says. “More importantly, they will be the companies that can replicate the competitiveness they developed in China overseas and build globally recognized brands.

“The future belongs not simply to the cheapest manufacturers, but to those that can turn China’s domestic strengths into sustainable international advantages.”

Enjoying what you’re reading?

Article Subscribe (1)

CKGSB Report

Related Articles

Our Programs

Scaling Innovation: AI and Digital Strategies for Business Transformation

Global Unicorn Program Series

In partnership with Columbia Engineering

This program is designed to equip senior executives with the strategic insights and tools necessary to lead in this transformative era.

LocationNew York, USA

Date27 Sep - 02 Oct, 2026

LanguageEnglish

Emerging Tech Management Week: Silicon Valley

Global Unicorn Program Series

In partnership with UC Berkeley College of Engineering

This program equips participants with proven strategies, cutting-edge research, and the best-in-class advice to fuel innovation, seize emerging tech developments, and catalyse transformation within your organization.

LocationUC Berkeley

Date01 - 06 Nov, 2026

LanguageEnglish

Asia Start (15th Edition): AI + Digital China Expedition

Asia Start provides entrepreneurs and executives with unparalleled access to Asia’s dynamic digital economy and its business ecosystems, offering the latest trends and insights, strategies, and connections to overcome challenges and unlock future growth for your business in Asia and beyond.

LocationChina (Beijing, Shanghai, Hangzhou & optional Shenzhen)

DateNovember 2-7, 2026

LanguageEnglish

Intelligent China: AI, EVs & Advanced Manufacturing

Participants may join the full 12-day journey or select individual modules based on their interests and priorities.

LocationBeijing, Shanghai & Hangzhou

Date12 Days

LanguageEnglish

Stanford & Silicon Valley Immersion Program

Global Unicorn Program Series

In partnership with Stanford Engineering Center for Global & Online Education

This CKGSB program equips entrepreneurs, intrapreneurs and key stakeholders with the tools, insights, and skills necessary to lead a new generation of unicorn companies.

LocationStanford University Campus,

California, United States

Date06 - 11 Dec, 2026

LanguageEnglish with Chinese Translation