CKGSB Business Conditions Index: Waning Optimism in China

March 02, 2016

CKGSB’s Business Conditions Index shows that Chinese business executives are even less optimistic than before.

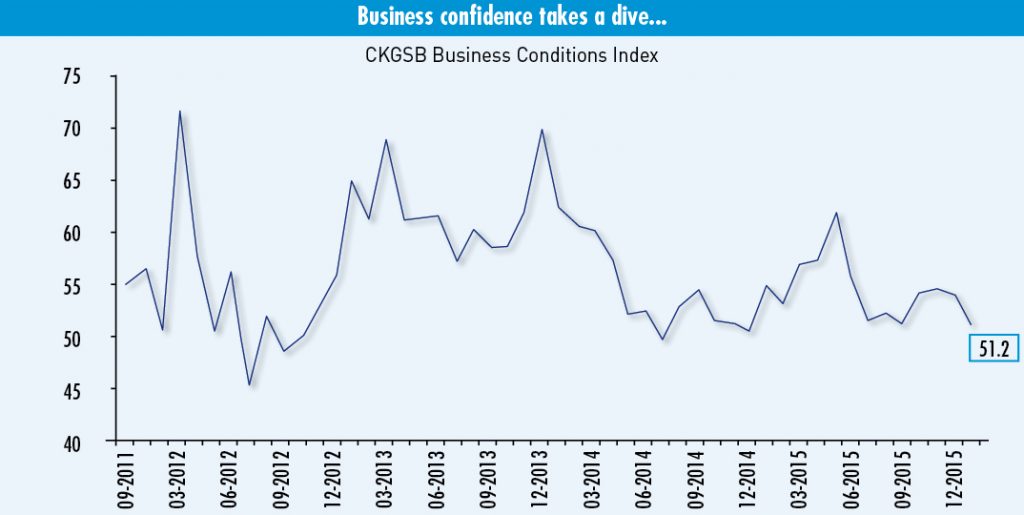

In January, the CKGSB Business Conditions Index (BCI) posted a figure of 51.2, a slightly lower overall reading than the previous monthly reading of 54.0 and slightly above the confidence threshold of 50. In May 2015, the BCI was at a considerably higher level of 61.3, but from July to September it was only just above 50. From October until December, the overall index has hovered around 54, but it has now slipped back towards the confidence threshold. This shows that for the majority of relatively successful firms in China, optimism about business conditions over the next six months is waning, and the current forecast for business operations is cautious optimism.

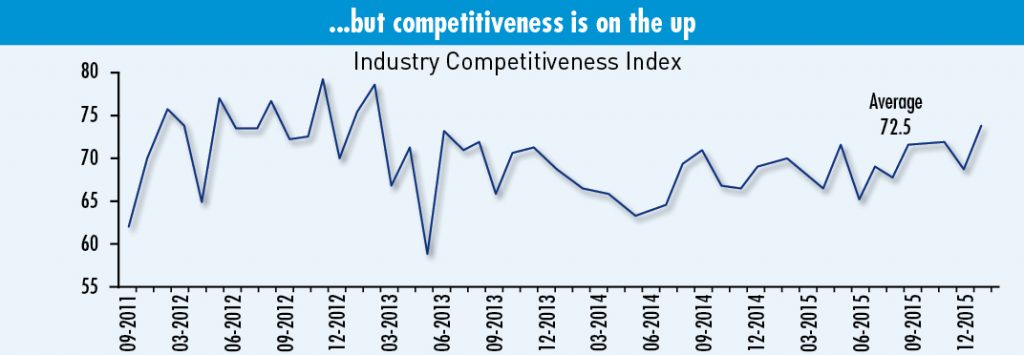

The BCI, directed by Li Wei, Professor of Economics at the Cheung Kong Graduate School of Business, asks respondents to indicate whether their firm is more, the same, or less competitive than the industry average (50), and from this we derive a sample competitiveness index (see Industry Competitiveness Index). As our sample firms are in a relatively strong competitive position in their respective industries, the CKGSB BCI indices tend to be higher than government and industry PMI indices.

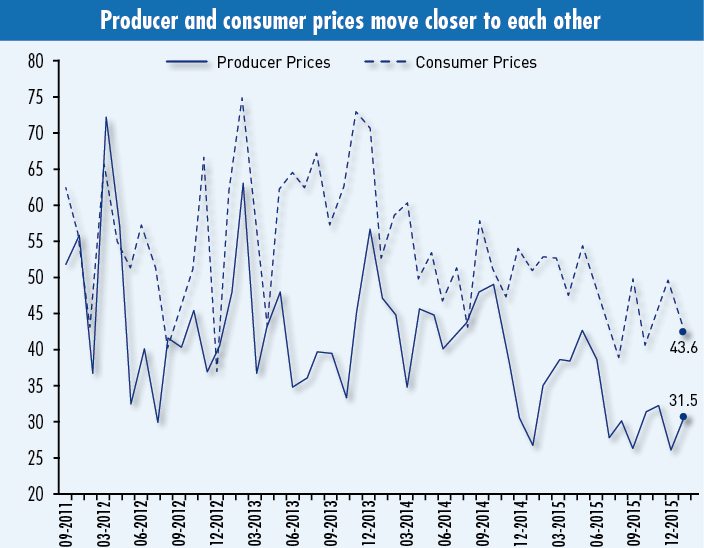

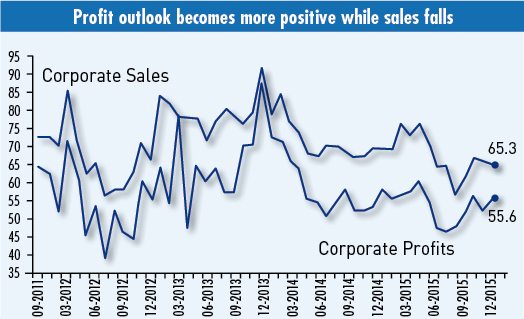

The consumer prices index fell from 50.0 to 43.6, and producer prices continued to hover at a low level, edging up from 27.8 to 31.5. Since January 2014, consumer prices have looked comparatively healthier and been mostly above 50, however the situation has deteriorated markedly, with the future trend unclear. Corporate sales fell from 66.3 to 65.3 in January, but the profit index rose, from last month’s 53.4 to this month’s 55.6. Although in recent months a sharp decline has been seen, this year profits expectations returned to over 55, showing that the profit outlook is becoming more positive for the upcoming six months. The labor demand index fell from 66.0 to 65.0—it has only been between 50 and 60 twice, and has remained above 60 for the rest of the time.

Enjoying what you’re reading?

Article Subscribe (1)

CKGSB Report

Related Articles

Our Programs

Scaling Innovation: AI and Digital Strategies for Business Transformation

Global Unicorn Program Series

In partnership with Columbia Engineering

This program is designed to equip senior executives with the strategic insights and tools necessary to lead in this transformative era.

LocationNew York, USA

Date27 Sep - 02 Oct, 2026

LanguageEnglish

Emerging Tech Management Week: Silicon Valley

Global Unicorn Program Series

In partnership with UC Berkeley College of Engineering

This program equips participants with proven strategies, cutting-edge research, and the best-in-class advice to fuel innovation, seize emerging tech developments, and catalyse transformation within your organization.

LocationUC Berkeley

Date01 - 06 Nov, 2026

LanguageEnglish

Asia Start (15th Edition): AI + Digital China Expedition

Asia Start provides entrepreneurs and executives with unparalleled access to Asia’s dynamic digital economy and its business ecosystems, offering the latest trends and insights, strategies, and connections to overcome challenges and unlock future growth for your business in Asia and beyond.

LocationChina (Beijing, Shanghai, Hangzhou & optional Shenzhen)

DateNovember 2-7, 2026

LanguageEnglish

Intelligent China: AI, EVs & Advanced Manufacturing

Participants may join the full 12-day journey or select individual modules based on their interests and priorities.

LocationBeijing, Shanghai & Hangzhou

Date12 Days

LanguageEnglish

Stanford & Silicon Valley Immersion Program

Global Unicorn Program Series

In partnership with Stanford Engineering Center for Global & Online Education

This CKGSB program equips entrepreneurs, intrapreneurs and key stakeholders with the tools, insights, and skills necessary to lead a new generation of unicorn companies.

LocationStanford University Campus,

California, United States

Date06 - 11 Dec, 2026

LanguageEnglish with Chinese Translation