The silver economy: why Chinese companies are chasing older consumers

April 20, 2026

Amid a slowing economy, the silver economy is providing a respite

As China’s economic growth slows amid weak domestic consumption, the demographic decline may provide an opportunity with the silver economy

China’s largest private education provider, New Oriental, is undergoing a surprising reinvention. Once synonymous with after-school tutoring for children across the country, the company is now pivoting towards the silver economy—that is, it is offering study courses for retirees in subjects such as digital literacy, culture and lifestyle enrichment.

The move follows a ban on for-profit tutoring in 2021. However, this is more than just a corporate survival strategy. It comes as China is grappling with the largest demographic decline since records began, as well as a slowing economy suffering from weak domestic demand. As young people face job insecurity and stagnant wage growth, businesses—such as New Oriental—are increasingly turning to older consumers as a more stable source of demand.

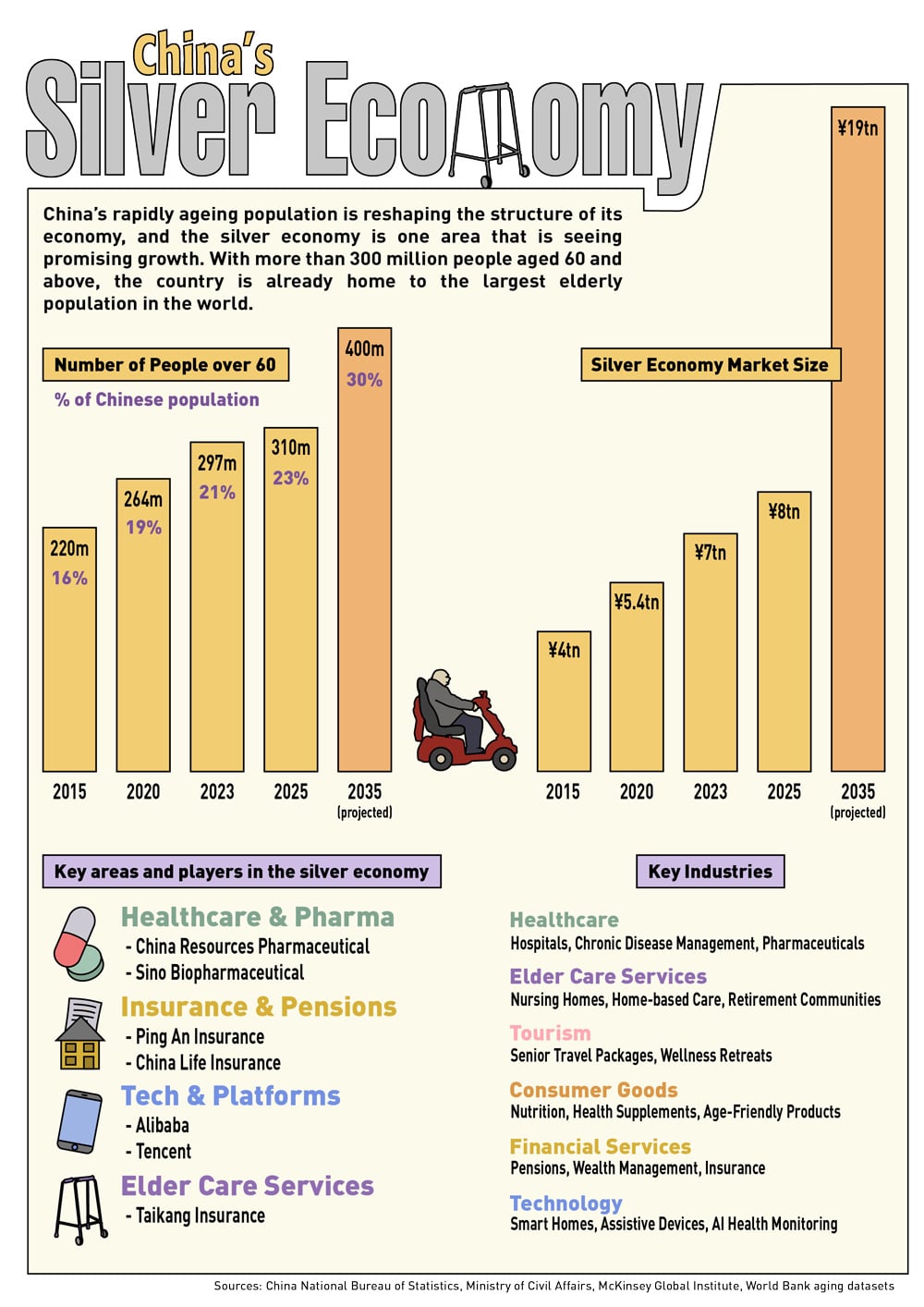

Estimates suggest the silver economy, including not only education, but also property, services, etc., is already worth around ¥7 trillion and is projected to grow to up to ¥30 trillion by 2035, accounting for as much as 10% of the GDP and nearly 28% of total consumption. With policymakers touting the importance of a rebalance of an economy overly focused on exports, retirees are emerging as a promising sector for boosting domestic consumption.

Yet the rise of the silver economy also raises the deeper question of whether such an ageing demographic can be the engine of sustainable growth. “The silver economy is partly a response to economic pressure, but even more fundamentally, it is a response to demographic inevitability,” says Zhao Litao, Senior Research Fellow at the National University of Singapore’s East Asian Institute.

A country in demographic decline

China is ageing at a rapid pace: By the end of 2025, the country had more than 320 million people aged 60 and above, within a population of 1.41 billion, with projections suggesting this will reach more than 400 million by the mid-2030s, while the overall population is not expected to change significantly. At the same time, the working age population is shrinking, and 2025 saw the lowest birthrate since records began—5.63 per 100 people.

As the demographic profile of China shifts, so too does the composition of demand. “As the proportion of over-60s rises sharply, the pattern of consumption will undoubtedly change… more spending on health, travel and services, and less on durable goods,” says George Magnus, research associate at the China Centre in Oxford University, and author of The Age of Ageing: How Demographics are Changing the Global Economy and Our World.

Older consumers are also staying economically active for longer. Improvements in healthcare and a rising life expectancy mean retirees today are healthier and more engaged than previous generations. Many are willing to spend on services that enhance quality of life, such as leisure travel and education.

However, spending power is not uniform across the country. China’s pension system remains fragmented, with relatively generous benefits for urban retirees—in particular those from the state sector—while rural residents and migrant workers often rely on far more limited support.

“China does not have one silver economy, it has several,” says Zhao. “The real divide is not just age, but age plus income, assets, hukou [household registration] and pension status.”

Consumption under pressure

The growing focus on older consumers also reflects broader weakness in domestic demand. China has long sought to rebalance its economy towards consumption, but progress has been uneven. A prolonged downturn in the property market has eroded household wealth and confidence, encouraging families to save more. At the same time, younger workers are facing rising job competition and slower wage growth, limiting their ability to spend.

This has left businesses searching for more reliable sources of demand. The service sector for older people, in particular, is emerging as one key area for expansion.

“Consumer-sector companies are leaning on this cohort not merely as a supplement, but as a strategic hedge,” says Alicia García-Herrero, chief economist for Asia Pacific at Natixis. Companies are, she says, “reallocating resources towards seniors, who are proving more reliable and often more willing to spend on health, leisure and convenience.”

But the extent to which the silver economy can really compensate for weaker consumption elsewhere remains uncertain. “The key point is that silver consumption is not a full substitute for weaker spending by younger cohorts… it is usually a partial offset, not a wholesale replacement,” says Zhao.

Silver services: the bigger picture

The silver economy spans a wide range of industries and is continuously evolving.

“The medical and care industries are at the core of the silver economy,” says Zhao, pointing out that demand will increasingly concentrate in practical, necessity-driven areas such as rehabilitation and home-based services.

Housing solutions, such as retirement communities and home modifications, are also emerging as areas of growth.

The financial sector is also taking advantage of the opportunities in the silver economy, with products covering wealth management, insurance, and inheritance planning consultations.

At the same time, wellness and fitness services are expanding as older consumers seek to maintain active lifestyles. Education and enrichment represent another growing segment—as seen with New Oriental’s pivot.

Tourism tailored to older travellers is also gaining traction, with companies offering itineraries which are slower-paced and take into consideration the needs of elder tourists.

A ready pool of demand

One of the key attractions of the silver economy for businesses is that spending power already exists. Many urban retirees benefit from relatively stable pensions and high rates of home ownership, having accumulated their wealth during the decades of rapid economic growth. As a result, they are well placed to spend money on quality-of-life consumption, such as wellness, dining and leisure.

García-Herrero points out that there is a stark contrast, however, between urban and rural or lower-tier city retirees, with urbanites spending up to 1.5 times more than their rural counterparts. “Urban, wealthier, pension-supported seniors are the real drivers: they travel, adopt smart devices, invest in wellness and prioritize enjoying old age,” she says.

Older members of China’s population are especially tech-savvy when compared to similar cohorts in other cultures. Elder Chinese tend to be comfortable using smartphones, mobile payments and online platforms. This enables new business models in areas such as online education, telemedicine and e-commerce.

Demand for technology may therefore become a growth driver itself. “The demands of older people for technology-related goods and services… could itself be a spur for demand in the economy,” says Magnus.

Uneven viability

As García-Herrero already pointed out, there is a large gap between urban and rural retirees. “Rural and lower-income elderly concentrate on essentials—food, basic medical needs—with far less access to or benefit from silver-economy innovations,” she says, pointing out that pension disparities exacerbate this. “Stable urban pensions enable independent spending, while rural or minimal pensions force heavy reliance on family support,” she says.

Another challenge lies in the blurred boundary between commercial services and social welfare. Many aspects of elder care are still shaped by public systems. While policy support is expanding, affordability and access remain key constraints, especially outside major cities.

Perhaps the most fundamental limitation of the silver economy is its relationship to productivity. While it can support service-sector growth, it does little to generate the productivity gains that are conducive to economic expansion.

“China’s strong policy emphasis on the silver economy comes at a time when traditional growth engines have weakened,” says Zhao. But he points out that this is only half the story. “The demographic driver is real and irreversible” China is not inventing ageing demand because the economy is weak; it is trying to organize an economic response to a social reality that is already here,” he says.

Demographics are destiny

As China confronts the twin pressures of demographic ageing and economic slowdown, the silver economy is both an opportunity and a necessity. For companies like New Oriental, it offers a pathway to adapt. For policymakers, it provides a tool to support consumption at a critical moment.

Demographics alone ensure that the sector will continue to expand. But its rise also reflects a deeper shift: China’s consumer sector is moving towards older spenders rather than expanding through younger and more dynamic ones. Spending by retirees can help stabilize demand, but it cannot replicate the younger consumer base, which tends to drive new industries, faster consumption cycles and productivity gains.

“Demographics, they say, are destiny,” says Magnus. “The presumption is that we cannot prevent the effects of rapid ageing on the economy,” he says. “This does not need to be the case if policy can address the consequences of rapid ageing of the workforce.”

Enjoying what you’re reading?

Article Subscribe (1)

CKGSB Report

Related Articles

Related Articles

Our Programs

Scaling Innovation: AI and Digital Strategies for Business Transformation

Global Unicorn Program Series

In partnership with Columbia Engineering

This program is designed to equip senior executives with the strategic insights and tools necessary to lead in this transformative era.

LocationNew York, USA

Date27 Sep - 02 Oct, 2026

LanguageEnglish

Emerging Tech Management Week: Silicon Valley

Global Unicorn Program Series

In partnership with UC Berkeley College of Engineering

This program equips participants with proven strategies, cutting-edge research, and the best-in-class advice to fuel innovation, seize emerging tech developments, and catalyse transformation within your organization.

LocationUC Berkeley

Date01 - 06 Nov, 2026

LanguageEnglish

Asia Start: AI + Digital China Expedition

Asia Start provides entrepreneurs and executives with unparalleled access to Asia’s dynamic digital economy and its business ecosystems, offering the latest trends and insights, strategies, and connections to overcome challenges and unlock future growth for your business in Asia and beyond.

LocationChina (Beijing, Shanghai, Hangzhou & optional Shenzhen)

DateNovember 2-7, 2026

LanguageEnglish

Stanford & Silicon Valley Immersion Program

Global Unicorn Program Series

In partnership with Stanford Engineering Center for Global & Online Education

This CKGSB program equips entrepreneurs, intrapreneurs and key stakeholders with the tools, insights, and skills necessary to lead a new generation of unicorn companies.

LocationStanford University Campus,

California, United States

Date06 - 11 Dec, 2026

LanguageEnglish with Chinese Translation