A Pivot South: China’s record trade surplus looks to developing markets

March 31, 2026

China’s exports are seeing a noticeable shift to the Global South. But the strategy raises questions about how long the model can last

Is China’s export shift to the Global South sustainable?

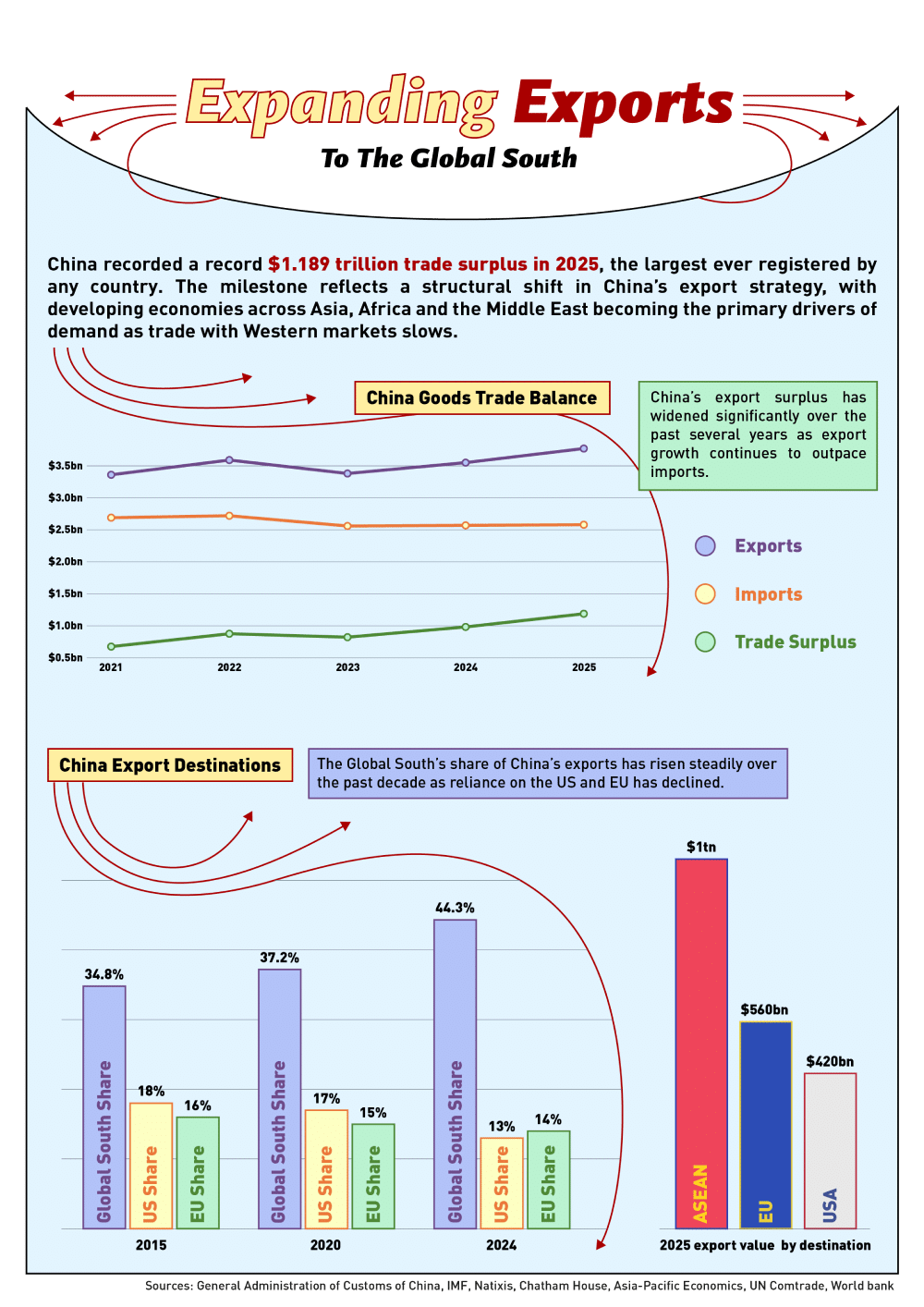

In 2025, China recorded a record full-year trade surplus of almost $1.2 trillion. The milestone—a figure on par with the GDP of Saudi Arabia—came on the back of an export surge toward the Global South as China continues to pivot away from Western-dominated markets and deepens ties with emerging economies.

Chinese exports in 2025 accelerated by 6.1% to $3.77 trillion, with imports remaining almost flat at $2.58 trillion, leaving a surplus of $1.189 trillion. “With a more diversified set of trading partners and significantly enhanced resilience against risks, the fundamentals of China’s foreign trade remain solid,” Wang Jun, a vice minister at China’s customs administration, said in January. Exports have remained resilient in 2026, expanding by more than 20% over January-February.

Probably even more significant than the export surge is the destination of the goods. China’s shipments to the US in 2025 slumped by 20% from 2024 to $420 billion, according to Chinese customs data. Exports to the EU stood at $560 billion, up by 8.4% from $516.5 billion in 2024.

But it is the Global South that is powering China’s export juggernaut amid rising protectionism in Western markets. The term Global South refers to developing countries and emerging markets in Africa, Latin America, the Caribbean, and Asia, which currently import from China 50% more than the US and Western Europe combined, according to S&P Global.

“The Global South has fundamentally transformed from being merely a source of raw materials to becoming China’s export lifeline—and frankly, Beijing’s economic insurance policy against Western containment,” says Alicia García-Herrero, chief economist for Asia-Pacific at Natixis.

A deeper question also underpins the shift: can emerging markets truly replace the US and Europe as the foundation China’s export model any time soon? Or are they for now to a large extent an intermediary in a system of transiting goods on to the West?

Made in China

The Chinese economic success story of the past few decades was built on exports to the US and Europe over decades, and it remained in pole position for all but one of the following 24 years. American and European dependency on imports sourced from China was founded on demand for consumer electronics, apparel, and cheap, low-value goods, helping made-in-China carve out an outsized weight in global production and trade.

In recent years, though, both the US and the EU have been less welcoming of Chinese trade as geopolitics have become increasingly polarized. Protectionism in both markets has increased alongside a growing sense that trade with China is no longer complementary—especially as Chinese manufacturers have ascended the value chain and now compete with American and European businesses in a growing variety of advanced industries.

China has leaned on its Belt and Road Initiative (BRI), launched in 2013 to develop alternative markets. Trade with BRI partners—the majority of which comprise the Global South—, an annual increase of 6.3% and representing 51.9% of China’s total foreign trade, hitting ¥23.6 trillion in 2025.

“This isn’t marginal diversification—this is a complete reorientation of China’s economic strategy,” says García-Herrero. “For the first time, these markets have collectively absorbed the damage from double-digit export declines to the US and sluggish EU growth.”

China’s growing trade with Global South nations is reflective of strong economic growth in many developing countries across South Asia and Southeast Asia, Africa, and the oil-exporting Gulf states of the Middle East. Total Chinese exports to the Global South jumped to 44.3% in 2025 from 37.2% IN 2020, according to financial data provider S&P Global.

“This has provided important diversification of export markets for China at a time when bilateral trade with the US has been severely impacted by US tariff wars and economic sanctions,” says Rajiv Biswas, CEO of Asia-Pacific Economics and author of Emerging Markets Megatrends.

The trade traffic has been one-way, as Biswas says the sustained strength of China’s economic expansion has also provided an important expanding growth for Global South exports, ranging from agricultural commodities, minerals, energy products, and manufacturers.

But the situation may be more nuanced than simply the Global South absorbing Chinese exports previously bound for the US or Europe, because a lot of these goods may transit on to other places.

“One way to think about the US tariffs is that they didn’t result in trade destruction but instead created trade diversion,” says David Lubin, a senior research fellow at British think tank Chatham House. “The suspicion must be that China is either using third countries to reroute goods to the US, or China may be using manufacturing facilities in third countries as a base from which to sell more stuff to the US,” says Lubin.

A similar pattern is apparent for other countries that channeled Chinese goods into the US at the height of the first Trump administration’s trade war with China in 2018-2019. “US tariffs have created what I call ‘tariff arbitrage on steroids’,” says García-Herrero, who points to Vietnam as an example. China’s neighbor is now a top-five export destination for Beijing—its trade deficit with China doubling to $98 billion since 2020.

“Let’s call it what it is: Vietnam has become China’s tariff-laundering hub. Chinese components flood in, get minimally assembled, and ship out with ‘Made in Vietnam’ labels. Hanoi is caught between benefiting from manufacturing relocation and becoming economically colonized by its giant neighbor,” says García-Herrero.

Winning the Global South

China’s future-facing industrial policy focused on the so-called ‘new three’—electric vehicles (EVs), lithium batteries, and solar photovoltaic technologies—has created genuine technological advantages that align perfectly with the Global South’s infrastructure needs and climate ambitions.

“The global energy transition has created strong growth in demand for China’s manufactures related to renewable energy generation, such as solar panels and wind turbines,” says Biswas. The sharp surge in global oil prices in reaction to the present crisis in the Middle East is likely to accelerate the move toward clean energy technologies too—particularly among Global South nations that have less ability to withstand commodity price shocks.

“Many developing countries, particularly in Asia, have significant oil and liquefied natural gas imports from the Middle East, so the transition away from oil and gas toward renewables helps to reduce vulnerability to oil and gas price volatility and supply disruptions,” Biswas says.

But Beijing’s burgeoning trade with the Global South has not been an unvarnished success story. Widening trade surpluses with emerging economies in Africa, the Middle East and ASEAN reflect how China mostly imports low-value primary products—natural resources such as agricultural goods, fossil fuels, and critical minerals and metals—while mainly exporting higher-value finished goods.

The structural trade surpluses have undercut the official Chinese view that its purchases of raw materials are producing prosperity across the Global South. Heightened economic tensions with trade partners are complicating Beijing’s geopolitical agenda. “The result is that the Global South is now the fastest-growing source of hostile trade policy actions directed at China,” says Lubin.

One example is Brazil, which has imposed tariffs on Chinese steel and launched investigations into rising EV imports.

Even heavyweight emerging economies like India have struggled to redress the trade imbalance. Despite all of New Delhi’s efforts to reduce dependence on China, the country’s trade deficit hit $115 billion in 2025, against total bilateral trade of $155 billion. “Why? Because India’s manufacturing ambitions require Chinese industrial inputs that nobody else can supply at competitive prices. Modi’s ‘Make in India’ increasingly means ‘Make in India with Chinese components’,” says García-Herrero.

Shifting the balance

China is betting that greater trade with the Global South will offset the impact of slower or reduced trade with Western markets, but it may not be sustainable, says García-Herrero, who argues that structural flaws in the Chinese economy also precipitated the pivot.

Domestic consumption remains stubbornly weak, with household spending equivalent to only 40% of GDP in 2024, compared with 60% across the nations in the Organisation for Economic Co-operation and Development in 2022.

“When your own consumers won’t buy your products, you have two choices: reform your economy or flood foreign markets,” says García-Herrero. “Beijing chose door number two, and the result is massive ‘overproduction’ that’s being dumped into Global South markets at prices that don’t reflect true production costs.”

The outcome is that Chinese manufacturers are caught in a vicious cycle because the Chinese economy is slowing, consumer spending is tenaciously low, and so their only resort is to continue exporting at a loss.

One advantage, though, is that with China selling affordable high-tech goods, it is simultaneously embedding its technological DNA into the developing world’s infrastructure. As Chinese firms export sixth-generation network equipment, clean energy grids, and high-speed rail to the Global South, they are not just winning contracts but also locking in technical standards for generations.

“Trade is very important for the diffusion of various international standards,” says Lubin. “An important concept concerning international trade is alignment. When many countries think the same way about macroeconomic policy, regulatory standards, or trade policy, you get maximal alignment and a convergence in trade.”

Additionally, where their products and services are incompatible with non-Chinese technology, Chinese manufacturers can effectively lock countries into purchasing any future upgrades from China. Beijing has been methodical about this—108 mutual recognition agreements with 65 partners worldwide as of early 2025 have helped position Chinese technical standards as potential regional defaults, while the China Standards 2035 initiative also is not subtle about its ambitions to move the country from being a ‘standards taker’ to a ‘standards maker’.

As China’s presence in the Global South trade grows, a gradual erosion of the West’s role as the default in global norms may be in progress. This may carry friction between the Global South and the West, which is important in all sorts of ways, including financial and political.

“To a large extent, this transition away from the US and EU toward the Global South has already transformed China’s pattern of trade, with the Global South already accounting for almost half of China’s exports,” says Biswas.

Headed south, but for how long?

China’s trade numbers last year in the face of escalating US tariffs would suggest it is succeeding in pivoting to the Global South. However, it appears as though China’s pivot is less a simple replacement of Western demand than a shift in global trade flows. The Global South is receiving more Chinese exports, but in many cases is also redistributing them. Still, the strong growth in many corners of the Global South, from Turkey to Brazil and India, suggests Beijing’s bet that emerging markets can replace the US and EU as the bedrock of China’s exports remains in play.

“In the past, I would have been pessimistic because I previously would have said that developing countries rely a lot on globalization as a basis for their ability to grow,” says Lubin. “But we’re now in a world where deglobalization has reared its head, but actually, it’s possible to be quite optimistic about growth in the developing world. That bodes well for China’s strategy.”

Perhaps the bigger issue is what the switch says about the sustainability of China’s export-oriented economy. While the trillion-dollar surplus impresses in headlines, it points to an economic model that García-Herrero believes is distorted and headed for a reckoning. “The current trajectory is fundamentally unsustainable, and the cracks are already showing,” she says.

“The model that produced the 2025 numbers isn’t built to last—it’s built on subsidies, overcapacity and increasingly fragile market access. Something has to give.”

Enjoying what you’re reading?

CKGSB Report

Related Articles

Our Programs

Asia Start: AI + Digital China Expedition

Asia Start provides entrepreneurs and executives with unparalleled access to Asia’s dynamic digital economy and its business ecosystems, offering the latest trends and insights, strategies, and connections to overcome challenges and unlock future growth for your business in Asia and beyond.

LocationChina (Shanghai, Hangzhou, Shenzhen)

Date11 - 14 May, 2026

LanguageEnglish

Scaling Innovation: AI and Digital Strategies for Business Transformation

Global Unicorn Program Series

In partnership with Columbia Engineering

This program is designed to equip senior executives with the strategic insights and tools necessary to lead in this transformative era.

LocationNew York, USA

Date27 Sep - 02 Oct, 2026

LanguageEnglish

Emerging Tech Management Week: Silicon Valley

Global Unicorn Program Series

In partnership with UC Berkeley College of Engineering

This program equips participants with proven strategies, cutting-edge research, and the best-in-class advice to fuel innovation, seize emerging tech developments, and catalyse transformation within your organization.

LocationUC Berkeley

Date01 - 06 Nov, 2026

LanguageEnglish

Stanford & Silicon Valley Immersion Program

Global Unicorn Program Series

In partnership with Stanford Engineering Center for Global & Online Education

This CKGSB program equips entrepreneurs, intrapreneurs and key stakeholders with the tools, insights, and skills necessary to lead a new generation of unicorn companies.

LocationStanford University Campus,

California, United States

Date06 - 11 Dec, 2026

LanguageEnglish with Chinese Translation