Will Ant Financial Become Wildly Successful Like Taobao?

May 24, 2016

With its revolutionary business model, Alibaba’s Ant Financial has grown to a $75-billion company in just three years. Going forward, how will it shake up China’s financial industry and possibly the world’s?

It was Li Weitang’s fourth month in his first job when he bought his first financial product: Yu’ebao, the money market fund sold by Alibaba’s Ant Financial, currently the most valuable tech firm in China.

But it took a while before the recent graduate realized that he had actually made an investment: he had simply transferred money to Yu’ebao from his Alipay account, a payment tool also owned by Ant Financial.

As a frequent shopper on Taobao, China’s largest e-commerce platform, 25-year-old Li is used to putting money in Alipay. When he heard it could earn him some money with Yu’ebao, he immediately opened the Alipay app and moved the money to Yu’ebao. The transaction is free and the whole process took no more than one minute.

By putting RMB 5,000 in his Yu’ebao account, Li would receive around RMB 0.4 every day. He is much wiser after this experience. “It’s a small amount, but it helped me start to think about investment,” he says.

Li is just one of millions of young people in China who frequently shop online and have grown to trust Alipay, Alibaba’s Paypal-like online payment platform. Youngsters like Li, who haven’t studied finance and don’t have prior knowledge or experience of investing, have found an easy way to earn small change, not through complicated fixed deposits in banks but by simply clicking on mobile apps.

Ever since it debuted in June 2013, Yu’ebao has lowered the investment threshold thus turning many non-investors into investors. The minimum deposit for Yu’ebao is RMB 1. In contrast, when you buy financial products from a bank in most cases the minimum threshold is RMB 50,000, which pushes aside several potential investors who don’t have much to spare. Besides, in the case of banks it often takes at least three months to receive the yield while in Yu’ebao, you can see the daily yield and withdraw the money at any time.

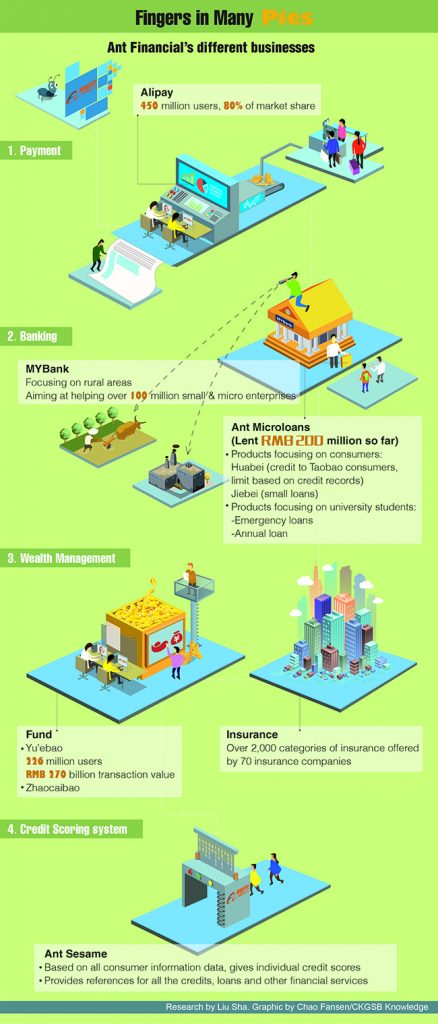

It’s no wonder then that Yu’ebao is revolutionizing China’s financial industry. Despite the fact that it mostly attracts small, micro and low-income investors, Yu’ebao has amassed over 260 million clients and RMB 711 billion in assets in just three years of existence. Tianhong Asset Management, sole operator of the Yu’ebao fund, has become China’s largest fund. A research done by Sootoo Institute says that 44.5% its users are between 20 and 29 year of age, and 39% are between the ages of 30 and 39, and the average balance is around RMB 5,000.

The Making of China’s Largest Fintech Company

Yu’ebao’s parent company Ant Financial is set to revolutionize the world of finance in China. Before we get into how, let’s take a look at how the company come about. Inspired by Paypal, Alibaba Chairman Jack Ma started Alipay in 2003 to provide an escrow service for the online shopping site Taobao. As Alipay’s users started increasing, he realized it could become a basic service for all online shopping activities. So Alipay was separated from Taobao in 2004 and it started operating on its own.

Alipay, which was initially connected with online shopping, was now being used in gaming, buying air tickets and even making daily payments like phone bills. By late 2011, it had become a mainstream online payment tool and that’s when it got a license for operating a fund.

Then in 2013, Alipay formally launched Yu’ebao and started accelerating its expansion into financial services. The fund promoted itself as the “fund for masses” saying that “we want to give you stable happiness and you can check your small gains every day.”

This was a big step for Alipay in changing its public image. Liang Yueping, Director of Ant Financial’s insurance division, told CBN Weekly that the development of Yu’ebao was an important milestone for Ant Financial, making people realize that Alipay is not just about online payments: it’s a tool you could use to manage your wealth.

Despite the fact that it targets small investors and its rate of return has been declining from a heady 7% to below 4% (which brings it closer to normal bank rates that are no more than 3% for five-year fixed time deposits), Yu’ebao is still the fund with the largest number of customers in China.

Officially known as Zhejiang Ant Small & Micro Financial Services Group, Ant Financial has built its own financial network: money market fund Yu’ebao, loans provider MYBank and Sesame Credit, a credit scoring system. Its over 400 million active users can access all these services with their Alipay account.

Split from e-commerce giant Alibaba in 2013, Ant Financial expanded at an unprecedented speed in the past three years and now it has an estimated market value of $75 billion, exceeding Uber, whose valuation was $51 billion. Recently, Ant Financial closed $4.5 billion in its second round of funding, the largest single private placement ever by an internet company globally, as the company said.

The company also plans to get listed on domestic A-share market in early 2017—likely to be China’s largest IPO since 2010 when the state-owned Agriculture Bank of China offered $22.1 billion worth of shares.

Given its explosive growth, it’s not hard to see why Ant is already one of the three most important businesses of e-commerce giant Alibaba Group—the others being the wildly popular Tmall and Taobao e-commerce platforms and logistics arm Cainiao network.

Focusing on the Little Guy

Just as the name “ant” indicates, the company focuses on the little guy. Song Min, Professor of Finance at Peking University, says that fintech companies like Ant Financial have seized the market that big Chinese banks and financial institutions have been ignoring: young people and low-income individuals who are potential investors.

Traditionally one has to go to a bank and open an account with a valid identity card and then select one or two wealth management products from a long list full of unfamiliar names and confusing data. Without knowledge of finance and an understanding of the fund market, this is not easy for the average Joe.

Song says that Ant financial has inherited the e-commerce way of thinking from Alibaba and more importantly, it has brought the e-commerce mindset into the finance industry. That is pushing traditional financial institutions to introspect and change their modus operandi from serving the manufacturing industry to serving consumers.

The e-commerce mindset has also influenced Ant Financial’s product portfolio. In 2015, Ant Financial became a shareholder of more funds and started an online bank, insurance services and formed crowd-funding site Antsdaq, after it got the country’s first equity-based crowd-funding license.

No doubt Ant has achieved tremendous success in the few years of its existence. But what does the future hold?

“In the future Ant Financial could become a [multi-service] financial institution and it can offer an online shopping platform for financial products, like Taobao, which does not own a single product but many shoppers operate on it,” Song adds.

In a written response to CKGSB Knowledge Ant Financial says that in the future it will be more than a platform for buying financial products. It will be an online social community of investors, with people sharing their investment experience and tips on it.

Since the company has also invested in China’s leading media firm China Business Network (CBN), professional economic and industry news and analysis can enrich the community’s content and provide investment references and guides, it says.

This strategy also responds to its biggest competitor—Tencent’s WeChat, which has over 650 million active users. Chinese people interact with WeChat more frequently than Alipay because it is a social networking tool.

“WeChat has grown tremendously in past couple of years, before people thought no company could take the place of Alipay. But Tencent has captured market share from Alipay by taking the platform approach…. The biggest challenge for Alipay when competing against Tencent is that they don’t have a platform [as popular as WeChat],” says Zennon Kapron, owner of Kapronasia Shanghai, a financial consulting and market research firm.

Ant’s core competitive advantage is big data: it has tons of data on the spending habits of consumers. It has collected it for years though Alipay and Taobao and that’s something that WeChat, which is more of a social media platform, lacks. Kapron says that with the shopping and payment data, Ant Financial can give loans and sell financial products based on big data, which helps them know their customers better to eliminate risk.

Into the Hinterland

Except for payment and wealth management, Ant Financial started online banking—MYbank, with registered capital of $644 million. It has issued different types of loans worth RMB 4.5 billion to over 800,000 small businesses, entrepreneurs and consumers by February 2016.

“The banking business has not grown as fast as the market expected. The general feedback we’ve got from people in the industry is that from a retail banking perspective, there is not too much incentive for people to use MYbank because a lot of functions they need are available on Yu’ebao,” says Kapron.

Kapron says that what average people use mobile banking for is still limited, plus most traditional banks have opened their apps and many people would find that enough.

So far people still cannot open accounts on MYbank because of two things. One is the regulatory authority’s concern over the facial-recognition technology that MYbank plans to use. Two, as Ant Financial’s chief information officer Tang Jiacai said, the bank will not rely on deposit.

Analysts in Shenzhen-based Essence Securities pointed out in an October 2015 report that the real significance of MYbank for Ant Financial and Alibaba is that it will build a foundation for finance and banking in China’s rural areas.

The decision has both economic and political significance, since there is a big market for finance in rural areas and the central government is focused on financially including rural areas an important part of its ongoing poverty relief campaign.

Data from the China Household Finance Survey conducted by Southwestern University of Finance and Economics showed that over 43% of rural family loans are disbursed through private lending and only 14% are from banks. Strong financing needs have been generated due to agriculture industry reform. In 2013, the government further eased land regulations to allow farmers to transfer their lands. As a result, farmers can now transfer their lands as shares to bigger companies, which can accelerate large-scale agricultural production. As Tencent’s Penguin Intelligence estimated, the land transfer could create a mortgage market worth over RMB 200 billion for fintech. Further mechanization of agriculture would generate an even larger market.

The government’s policy support is another incentive. The central government has set a target of 100% broadband coverage in the countryside. In the first policy document released in 2016, the central government also made it clear that the government encourages financial institutions to give more loans to agriculture businesses.

Xiaomi’s CEO Lei Jun also predicted that rural areas would be the next battlefield for tech companies in the coming decade. Ant Financial is not the only fintech company seeking to expand business in the countryside. E-commerce giant JD and asset management company Credit Ease have also made specific financial products for rural areas. But Ant Financial has leveraged the Taobao platform, along with Alibaba’s rural Taobao strategy, to give out loans and help agricultural businesses to set up stores on Taobao and Tmall. Meanwhile MYbank has also created credit loan Wang Nong Dai, in which the borrowers do not need provide any collateral and can borrow up to RMB 500,000 and pay back monthly installments via Alipay.

More importantly, Ant chose to work with Postal Savings Bank of China, which was one of Ant Financial’s shareholders and has the largest offline network in China’s towns and villages.

However, pushing financial services into rural areas is not easy. For one, many young people are moving to the big cities, leaving the elderly and kids in villages and towns who are not as familiar with finance as those living in urban areas.

Ant Financial has set for itself some concrete goals such as assisting in building ‘Taobao Villages’ nationwide. Taobao Villages are villages full of entrepreneurs whose sole focus is to produce goods and sell them online on Taobao. Ant’s goals are to encourage online start-ups, move local businesses online and help local business people get loans for their business from Ant Financial. But it will have to spend a lot time popularizing its business to people in rural areas and habituate them to use mobile banking, says Huang Zhen, finance law professor at Central University of Finance and Economics.

He adds that it is often hard to evaluate the risk of loans in rural areas, because many local people do not have a credit record. “Ant Financial has to rely on Taobao and Tmall to accumulate data.”

“If Ant Financial could help more farmers financially, it will also be a relief for government,” he says.

Aligning With the Government’s Goals

In the latest round of fundraising, several state-owned companies, including the China Investment Corp. Capital, China Life, China Post Group, the parent company of Postal Savings Bank of China and China Development Bank Capital, become major investors of Ant Financial.

Before 2011, Alipay was controlled by foreign capital through Yahoo and then it separated from Alibaba and became a purely domestic company. Now after the second round of fundraising, the company’s largest investors are state-owned enterprises (SOEs). Hangzhou-based China E-Commerce Research Center calls it a process of how Ant Financial is becoming more closely connected with the government. “Absorbing large SOE shareholders could reduce its financial risk to a certain extent,” it says.

In China, keeping close ties with SOEs means better communication with the government, getting to know about new policies and getting different licenses easily. This is especially important at a time when the country has tightened online financial businesses after the eruption of the Ezubao scandal, when the peer-to-peer broker cheated about 900,000 investors out of more than $7.6 billion. The company put fake projects on their company’s website to attract individual netizens to invest money.

While enjoying government support domestically, Ant Financial also nurses global ambitions. Just one week after its second round of fundraising, the company hired former Goldman Sachs banker Douglas Feagin to help the company’s global strategy.

It’s not surprising as CEO Jing Xiandong has said earlier that this round of fundraising will go to not only rural finance, but also to globalization of the company. Previously Ant has worked with South Korean companies to establish K-bank. In India it has injected cash in Paytm, a mobile payment and e-commerce platform, and acquired a 25% stake in Paytm’s parent One97 Communications.

But analysts are still looking forward to the second round of global investment since its moves so far are just increasing Ant Financial and Alibaba’s presence in the global finance market.

“This initial round of investment has mainly been focused on finding an international foothold and gaining some experience and insight into the markets. What will be interesting to see is how they are able to then integrate these investments into their existing businesses and if they are able to create a complete international banking and payments platform,” says Kapron.

Can Ant recreate its phenomenal success beyond China’s borders? That’s something we’ll have to wait to see.

Enjoying what you’re reading?

Article Subscribe (1)

CKGSB Report

Related Articles

Our Programs

Scaling Innovation: AI and Digital Strategies for Business Transformation

Global Unicorn Program Series

In partnership with Columbia Engineering

This program is designed to equip senior executives with the strategic insights and tools necessary to lead in this transformative era.

LocationNew York, USA

Date27 Sep - 02 Oct, 2026

LanguageEnglish

Emerging Tech Management Week: Silicon Valley

Global Unicorn Program Series

In partnership with UC Berkeley College of Engineering

This program equips participants with proven strategies, cutting-edge research, and the best-in-class advice to fuel innovation, seize emerging tech developments, and catalyse transformation within your organization.

LocationUC Berkeley

Date01 - 06 Nov, 2026

LanguageEnglish

Asia Start (15th Edition): AI + Digital China Expedition

Asia Start provides entrepreneurs and executives with unparalleled access to Asia’s dynamic digital economy and its business ecosystems, offering the latest trends and insights, strategies, and connections to overcome challenges and unlock future growth for your business in Asia and beyond.

LocationChina (Beijing, Shanghai, Hangzhou & optional Shenzhen)

DateNovember 2-7, 2026

LanguageEnglish

Intelligent China: AI, EVs & Advanced Manufacturing

Participants may join the full 12-day journey or select individual modules based on their interests and priorities.

LocationBeijing, Shanghai & Hangzhou

Date12 Days

LanguageEnglish

Stanford & Silicon Valley Immersion Program

Global Unicorn Program Series

In partnership with Stanford Engineering Center for Global & Online Education

This CKGSB program equips entrepreneurs, intrapreneurs and key stakeholders with the tools, insights, and skills necessary to lead a new generation of unicorn companies.

LocationStanford University Campus,

California, United States

Date06 - 11 Dec, 2026

LanguageEnglish with Chinese Translation