The Money Squeeze: China’s tightening Credit Market

May 01, 2013

The first signs of light emerge amidst the dark prospects for private enterprises in China’s ever-tightening credit market

It’s been a miserable few months for financing in China’s private sector. A growing number of debt defaults by companies has spurred regulatory crackdowns on the unofficial lending sector, sometimes called ‘shadow banking’, which has sustained (not in an entirely healthy way) the mainland’s private small and medium-sized enterprises (SMEs) for decades. The bloom is now off the rose of Wenzhou’s entrepreneurial miracle [see ‘Wenzhou For Everyone?’], and the expected expansion of infrastructure investment is likely to only deepen the lending skew toward state-owned enterprises.

The wall of issues facing the country’s large shadow banking sector came to a head in November when Hua Xia Bank clients took to the streets of Shanghai after the bank failed to pay returns on wealth management products totaling $22.5 million. These wealth management products are typically run as off-balance sheet lending by the banks, which by the state’s definition, is shadow banking.

There are even graver consequences than money loss when defaulting on an off-the-book lender, as Xue Jie, a lawyer with Shanghai DongDao Law Firm, says.

“If private loans are in default, the biggest problem is the person in charge can use various non-legal means, such as destruction of operations, or even threats to property and personal safety,” he says.

Private SMEs, with or without official assistance, must find a way to break out of the cramped financing space in which they’re currently operating if they are to free themselves of the risk-laden avenue of underground lending.

And cracks in the financial glass ceiling are emerging. Certain alternative financing methods are evolving, such as with the emergence of more scientific credit rating systems, foreign banks recommitting to SME services despite the recent conformation to the national loan-deposit ratio requirements, and micro-loans via peer-to-peer lending platforms online.

The potential success of any of these channels depends on commitment from the Chinese government. One such channel that has been relentlessly encouraged (even while controlled) is the issuance of corporate bonds. But just how viable an option it is for China’s SMEs is open to debate.

Bound Corporate Bond Market

The China Securities and Regulatory Commission (CSRC) has stated its support for SME financing, in addition to taking steps toward freeing up the corporate bond market. A statement published in the state-run People’s Daily in June iterated its intentions toward private placement bonds.

“As corporate bonds, the private placement bonds meet the market demand of high-yield bonds but are not limited to it. It is legal to issue such bonds and it also is conducive to improving the financing facilities and means of small and medium-sized enterprises,” the statement read.

But the question of corporate bonds being a viable option as a significant source of finance evokes staid responses, as some experts characterize the corporate bond market as hospitable primarily to state-owned enterprises (SOEs) and those contracted by the state.

“The issuance of corporate bonds is an unrealistic debt financing channel for SMEs,” says DongDao’s Xue. “There are strict restrictions in the issuing entity, offering amount, investment targets, interest rates, underwriting, raising methods and purposes.”

Liu Jing, Professor of Accounting and Finance at the Cheung Kong Graduate School of Business, explains that guaranteed corporate bonds mainly represent to investors a government-backed guarantee and a healthy relationship between the issuer and the guarantor, hence a corporate bond market that is still largely dominated by SOEs and local government financing vehicles. “Certainly there is potentially a strong future for it (the bond market), but it’s still dominated by the state,” says Liu.

For what it’s worth, there is a clear and obvious campaign from the central government to stimulate and diversify China’s corporate bond market. The CSRC released a draft of proposed regulation changes to the International Finance Review, a research arm of Reuters, resulting from a series of soft-market consultation rounds, the latest of which concluded in early February this year.

According to the draft, the CSRC plans to allow non-listed companies to sell bonds through corporate private placements and to shorten the minimum tenor of privately placed corporate bonds to less than a year. Whereas only SMEs could issue private enterprise bonds as of the first half of 2012, under the new guidelines, any issuer could issue corporate bonds.

This is good news for the nation’s fund-starved private SMEs who may not be deemed eligible for an IPO in China. Under existing rules, the issuer’s outstanding bonds should not exceed 40% of their net assets. Private bonds, however, will not be counted.

Activity in the corporate bond market has increased considerably in recent years, starting in 2007 when corporate bonds were opened to companies listed in China or abroad on a pilot basis, and ending most recently with the CSRC’s debut of the fast-tracking issuance approval in 2012 and initiation of a high-yield junk bond market that requires only registration.

Different sources give different figures to illustrate the resulting growth of the corporate bond market. CSRC Chairman Guo Shuqing, said in January that corporate bond financing increased by 60% to RMB 3.62 trillion in 2012. According to the International Finance Review, the amount of outstanding corporate bonds rose 33% year-on-year reaching RMB 738.9 billion as of November 2012.

But figures indicating the percentage of corporate bonds issued by private SMEs are nowhere to be found.

Tri Tech Holdings Inc., a Beijing-based wastewater treatment company was featured in a Forbes article in October as one private medium-sized enterprise that raised funds via corporate bond issuance.

Tri-Tech issued RMB 50 million of three-year bonds to investors, including financial institutions. But with a gross profit margin of 25.3% in September, revenue growth exceeding the industry average, and shares listed on Nasdaq, Tri-Tech bears little resemblance to other private SMEs, such as those comprising the 2011 Alibaba survey of 2,300 SMEs in Zhejiang Province showing more than 70% of respondent businesses recorded zero profits or small losses, and 3% closed down.

In addition, the Forbes report noted that Tri-Tech had a credit guaranteed from Beijing Capital Investment and Guarantee Co., which is controlled by the state. Exceptional as the Tri-Tech example may be, the state-sponsored underwriting of its corporate bond is indicative of a bond market still under the government’s direction.

No matter what liberalization measures the CSRC takes toward the corporate bond market, there is one domain the companies themselves have reign over that could make or break them in their investors’ eyes: information.

Shooting One’s Own Foot

Information asymmetry has been a buzzword in academic research conclaves dedicated to private sector development.

Zhou Wubiao, Assistant Professor of Sociology at Nanyang Technological University in Singapore specializing in private sector development research, iterated the ‘information asymmetry’ problem for financiers in China in a 2009 World Development Journal research report.

“Since entrepreneurs possess information about themselves and their opportunities that lenders do not possess, lenders face high risks when lending to entrepreneurs because entrepreneurs may behave opportunistically toward them,” he wrote.

Chinese companies have been marked as vastly ‘asymmetrical’ in this regard thanks to a number of high profile investment fraud cases in the US stock market and the more recent bout between the US Securities and Exchange Commission and the CSRC over refused access to certain work documents of US-listed Chinese companies.

Even in the Wenzhou reform climate of legitimizing traditionally unofficial lenders, there has been a rash of entrepreneurs securing loans from the accepted non-bank lenders and then skipping town. Each such case serves only to increase the hesitancy with which banks regard smaller enterprises, not to mention private investors.

Information asymmetry, and flat out dishonesty, is one among several obstacles preventing China’s private sector from fully optimizing some of the more globally common financing channels.

According to Alberto Forchielli, Founding Partner of Mandarin Capital Partners, it takes his team no more than a day to detect fraudulent information from a Chinese company targeted for investment or acquisition.

“If they tell a lie, we’ll find out in 24 hours,” says Forchielli. “You can be the best company in the world, but if you tell a lie, you’re finished.”

Facilitating foreign investment in SMEs is challenging in every part of the world, Forchielli notes, and building trust is the make or break criteria at the end of the day.

Beyond foreign investors, foreign banks are also a resource, which, if given fair access to China’s credit market, could up their contribution to the best of the SMEs trying to raise funds.

(Source: Financial Times, China.org, Standard Chartered, Bloomberg)

Banking Diplomacy

Foreign investment in China seems ever constrained by an intricate array of protectionist policies and regulations, but foreign banks are showing signs of willingness to embrace the opportunities. The year 2011 saw impressive profits for foreign banks in China, a total of RMB 16.3 billion, signaling more than double the profits year-on-year, but their share of the Chinese banking sector is achingly low. According to PricewaterhouseCoopers’ latest survey, 181 foreign banks in China hold just 1.93% of the market.

The good news is that as the foreign banks turn away from their original strategy of taking minority shareholdings in local China banks, there is greater incentive for foreign banks to redirect their investment into expanding their own shops.

The Australia and New Zealand Banking Group (ANZ) did just that last year when it backed out of its plan to inject $120 million into the Bank of Tianjin and instead invested $300 million of capital into its own China operations after mainland incorporation in 2010, according to an Australian Financial Review report.

If this kind of capital redirection trends upward, it could add resources to financing in China’s private sector. Generally speaking, the private sector in China, and SMEs in particular, should represent an irresistible opportunity for foreign banks. Their risk management and credit-rating systems are typically more developed and better equipped to handle the issue of information asymmetry than that of their local counterparts, plus, they hold the advantage in variety of financial products and international frameworks. The latter particularly benefits the export-oriented businesses, which many Chinese SMEs are. UK bank Standard Chartered Plc CEO Peter Sands told Bloomberg Television in March that export-oriented SMEs are their specialty and they do more lending than any other foreign bank in China. The bank expanded its SME loan book in the “other Asia Pacific” region, which includes China, by 17% to $5.79 billion, the bank said in a filing in February 2012.

Citibank China is another bank that has targeted China’s SMEs. In 2004, Citibank China announced service offerings targeting smaller private enterprises. In 2010, it announced a new service that would allow small enterprise entrepreneurs one-stop access to both commercial banking services and personal banking services through a single manager, said their statement on the launch in 2010.

According to a 2009 editorial from China Business Focus, foreign banks were chomping at the bit to build their SME business in China and take full advantage of their five-year buffer from the China Banking Regulatory Commission (CBRC). The CBRC gave foreign banks an additional five years starting in 2007 to meet the same loan-deposit ratio require¬ment of 75% or less that national banks had been heeding previously. Now into 2013 however, foreign banks have con¬tracted their lending in accordance with the regulation, and are seeking to com¬pensate by expanding wealth management services and inter-bank lending.

So it seems that we have a one-step forward one-step back scenario, but the five years of relative loan-deposit ratio freedom observed by foreign banks shed light on the goodwill and zeal existing between these banks and China’s SMEs, particularly along the Yangtze and Pearl river deltas, where many of the export-oriented SMEs are located.

Provided foreign banks can develop enough channels to up their deposits, there will seemingly be only more determination to tap China’s SME lending market. More branch operations would also be a welcome move for financial services firms that specialize in cross-border investments. “We try to stay away from getting local financing because it’s too burdensome, we’ll waste way too much time with it,” says Mandarin Capital Partners’ Forchielli, explaining that they’re “very discouraged” from seeking loans from local China banks due to an overly copious application and guarantee process.

However “burdensome”, the process has not yielded highly effective risk management systems in China’s big banks, though the lesser among them are starting to lead the way.

Hope from Minsheng Bank

One development this year that boosts hope for small and micro-sized firms is Minsheng Bank Corp’s seemingly successful prioritization of small and micro-sized firms. According to its latest earning report, Minsheng netted RMB 37.56 billion in profits, a 34.5% increase from 2011, and it did it on the back of small enterprises. China Daily reported 62% of Minsheng’s micro-lending were non-mortgage loans geared toward small businesses. The bank’s chairman, Dong Wenbiao, termed the sector a “deep blue sea”.

Another key development for Minsheng in 2011 was its partnership with FICO, a risk assessment and analytics service provider, to bring its risk management system up to speed with its active lending portfolio. The new system uses IT to quantify, and to some degree automate, the application risk grading process. The impact that such an update will have on its portfolio and lending activity hasn’t crystallized yet, but it does somewhat alleviate the issue of risk management officers having to defer, in many instances unwisely, to the will of managers and loan officers who are swimming in as many political directives as commercial interests.

Christopher Whalen, co-founder and Managing Director of Institutional Risk Analytics, noted in his 2007 editorial for the Global Association of Risk Professionals that credit risk is often bulldozed in Chinese lending institutions.

“If you take a senior risk management position at a Chinese bank, you had better be prepared to be ‘flexible’”, he wrote, going on to explain that ‘flexible’ means approving loans to the politically well-connected with slim to zero hope of seeing it paid back.

A data based and relatively computerized system like that of the newly minted system at Minsheng could relieve the pressure of such ‘flexibility’.

Another way to extricate good lending practices from political motivation is to legitimize private lending institutions, as we’ve seen in experimental form in the city of Wenzhou. But the reality of the legal implications of loan defaults have cast a shadow on the potential nationalization of Wenzhou reforms, which could result in leading entrepreneurs to even more alternative lending.

(Source: Bank of China, finance.com, fjsen.com, hexun.com)

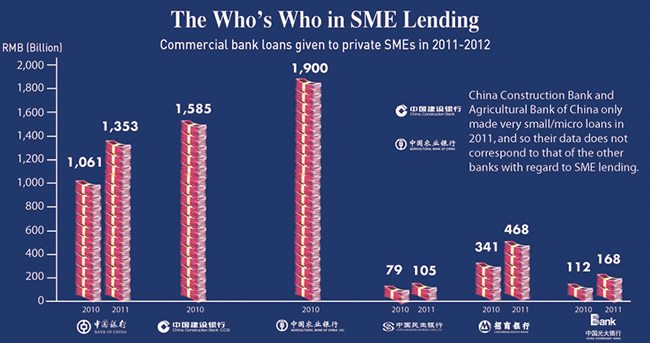

*The numbers represent the balance of loans given to SMEs at year’s end, and is inclusive of the previous year’s data

They Haven’t Said ‘No’ Yet

In March of 2012, China National Radio reported that more than 2,000 peer-to-peer (P2P) lending websites had been set up nationwide since 2007, with the value of their loans increasing 300-fold, reaching RMB 6 billion as of mid-2011.

The official response to the boom has been one of warnings rather than outlawing. Such was the basis for the go-ahead attitude of Ppdai.com’s founders, who were featured in a Bloomberg report in January.

“We went ahead because we couldn’t find any regulation that specifically bans it,” Zhang Jun said of his founding one of the nation’s largest P2P financing sites, in the report. The CBRC’s warning statement from September of 2012, asserted that the bad-debt ratio of these lending sites was “significantly higher” than that of banks, but an exact figure was not released.

P2P lending being outside of jurisdiction evokes inherent risks, such as lack of enforcement when a borrower defaults, but the same could be said of the shadow-banking sector, which has yet inspired great self-censorship from borrower or lender.

With Ppdai, borrowers give basic information and a proposal of their loan requests, investors review it and lend if they meet the criteria. Loan amounts start at RMB 3,000 and reach up to RMB 500,000 with interest rates supposedly not exceeding the legal 23%.

But a Ppdai representative tells CKGSB Magazine that one of their members recently raised only RMB 2,400 in three days on loans with an interest rate of 24%. Such figures represent micro-loans geared more toward self-starters than businesses with any real overhead expenses, plus, the complete lack of regulation is a red flag. The same representative says that if a borrower defaults on repayment, then their information and identity card will be posted on the site, a small comfort to the lender.

The Lending Ceiling

Whether lending pocket money online or bank capital, it all boils down to risk management, and with that, there is much banks can do themselves before hitting a wall.

According to Edward Tse, Chairman of Booz and Co. China, a global management consulting firm, scientific and quantitative approaches to credit rating and risk management are positive steps in the direction of a healthy private SME lending environment. But he also notes that as long as political influences impact loan officers, there is only so far any bottom-up reform will go.

“In a way there’s only so much you can do if you’re trying to drive this from a more internal management standpoint, banks have really been trying to improve their discipline and better their credit management systems, but really ultimately it’s the loan officers, not only in the bank, but also those out there in the provinces, making the decisions,” Tse says.

Liu Jing of CKGSB also complements the Minsheng approach, but adds a caveat.

“We need to reform the financial sector toward private enterprise to sustain China’s economic growth, but without reforming the ownership structure of the banks, that becomes very difficult,” Liu says.

Wenzhou for Everyone?

The March 2012 launch of the Wenzhou pilot financial reform zone had many a credit-starved entrepreneur celebrating what was potentially the first step along the path to an eased flow of capital and financial breathing room. The State Council brought lending institutions previously dubbed as ‘shadow banks’ into a regulated environment in the hope of bringing more liquidity to the nation’s SMEs.

Lately however, many small business owners have revealed true colors by neglecting the terms of repayment on their loans, or skipping town in the more severe cases. The result is an alarming increase in debt cases brought before the courts in the city, high enough in volume that much of the goodwill generated by Wenzhou in Beijing could wilt in response.

In February 2012, the Intermediate People’s Court and High People’s Court of Wenzhou handled 19,511 cases on private financing involving approximately $3.52 billion and settled 5,393 cases on financial lending disputes, China Daily reported. Should legal reform be coupled with financial reform, investors could feel freer with their money and debtors would have to think twice before simply locking the up the doors and speeding out of the city.

Enjoying what you’re reading?

Article Subscribe (1)

CKGSB Report

Related Articles

Our Programs

Scaling Innovation: AI and Digital Strategies for Business Transformation

Global Unicorn Program Series

In partnership with Columbia Engineering

This program is designed to equip senior executives with the strategic insights and tools necessary to lead in this transformative era.

LocationNew York, USA

Date27 Sep - 02 Oct, 2026

LanguageEnglish

Emerging Tech Management Week: Silicon Valley

Global Unicorn Program Series

In partnership with UC Berkeley College of Engineering

This program equips participants with proven strategies, cutting-edge research, and the best-in-class advice to fuel innovation, seize emerging tech developments, and catalyse transformation within your organization.

LocationUC Berkeley

Date01 - 06 Nov, 2026

LanguageEnglish

Asia Start (15th Edition): AI + Digital China Expedition

Asia Start provides entrepreneurs and executives with unparalleled access to Asia’s dynamic digital economy and its business ecosystems, offering the latest trends and insights, strategies, and connections to overcome challenges and unlock future growth for your business in Asia and beyond.

LocationChina (Beijing, Shanghai, Hangzhou & optional Shenzhen)

DateNovember 2-7, 2026

LanguageEnglish

Intelligent China: AI, EVs & Advanced Manufacturing

Participants may join the full 12-day journey or select individual modules based on their interests and priorities.

LocationBeijing, Shanghai & Hangzhou

Date12 Days

LanguageEnglish

Stanford & Silicon Valley Immersion Program

Global Unicorn Program Series

In partnership with Stanford Engineering Center for Global & Online Education

This CKGSB program equips entrepreneurs, intrapreneurs and key stakeholders with the tools, insights, and skills necessary to lead a new generation of unicorn companies.

LocationStanford University Campus,

California, United States

Date06 - 11 Dec, 2026

LanguageEnglish with Chinese Translation