The Infinity Loop

February 25, 2021

President Xi Jinping is reinventing state capitalism and has a new economic agenda: “Dual Circulation”. What does it mean for international trade and will it be successful?

The words “giant panda” have taken on a new meaning in the central city of Datong. A patchwork of dark and light solar panels glittering in the sun resembles nothing more than a standard solar farm from the ground. But from above the panel arrangement forms the image of a panda, the perfect representation of China’s bid for energy self-sufficiency.

Despite being the world’s biggest coal producer, China has long relied on other countries for its massive energy needs. It imported more than $238 billion-worth of oil in 2019 alone, around 60% of its total oil consumption. With international tensions rising and attitudes about globalization changing, this is one of many dependencies Beijing wants to reduce.

In May 2020, President Xi Jinping announced a new economic policy, “Dual Circulation.” While there has been much discussion over what it means, in its essence it is an attempt to rebalance the country’s economy away from relying on external forces and toward a more inward-facing system of production and consumption. Xi urged the nation to, “fully bring out the advantage of China’s super-large market scale and the potential of domestic demand to establish a new development pattern featuring domestic and international dual circulations that complement each other.”

Experts have extrapolated that to mean trying to reduce imports of strategically important items, particularly in the fields of energy and technology, and encourage citizens, companies and organizations to buy locally produced goods as much as possible. Manufacturers who have worked for decades to build export markets around the world are being told to now focus instead on the domestic market.

“The government has been talking about import substitution and domestic demand for 20 years, so I’m not surprised by the destination,” says Anne Stevenson-Yang, co-founder of research firm J Capital Research. “The question is, what are the policy measures to take it there?”

How did we get here?

Dual Circulation as a name is an echo of a policy proposed by the leadership in 1987—“international circulation economic development strategy”—when Beijing was desperate to expand its economic ties with the outside world by whatever means possible. The original policy, pushed by reformist leader Deng Xiaoping, correctly presumed that China could fund national development by using its low-cost workforce to develop export-intensive industries. In the following years, the country became the “world’s factory,” manufacturing a mind-boggling range of goods and shipping them across the globe.

But the limitations of an export-dependent system first appeared during the global financial crisis of 2008, when factory orders for a time dried up. Hu Jintao, Xi’s predecessor, proposed countering the crisis by expanding domestic consumer demand. The government rolled out a swathe of new policies to this end, including tax breaks for businesses supplying the domestic market and subsidies for farmers buying locally-made home appliances.

The trend was turbocharged in 2015 when Premier Li Keqiang launched the Made in China 2025 policy, a national strategy to move the country’s manufacturing sector higher up the food chain through a process of import substitution. By encouraging the local production of previously imported products and services, the goal is more independence from foreign suppliers in areas like biotech, energy and, crucially, the semiconductor chips vital for high-end electronics.

In recent years, the Chinese economy has been slowing. That, plus the trade war with the United States and the desire of many countries and companies to become less dependent on China supply chains, heightened by the COVID-19 pandemic, has made Beijing hyper-aware of its economic vulnerabilities. Having once seen global trade ties as a source of geopolitical and economic growth, China is being forced to consider the consequence of its own reliance on other nations. The US government’s punishment of Chinese tech champions like Huawei and ZTE for breaking sanction rules by denying them access to key US components and technologies has had a clear impact on thinking.

“The trade war initiated by the US has made China realize that it couldn’t rely on imports of key equipment and core technologies anymore,” Cong Yi, a professor at Tianjin University of Finance and Economics, told the state-run Global Times in July. “Hence, the country will surely ramp up its efforts to make key breakthroughs in bottleneck technologies such as semiconductors and high-end manufacturing.”

Other countries in the region, most notably Japan and South Korea, which created the blueprint for economic development, have already shifted their economies from export-focused to domestically led. China now has a rapidly growing middle-class, calculated to be at least 400 million-strong, increasingly willing to buy local products. The difference is however, that Japan and South Korea had ready reached a general level of prosperity when exports began to fade in importance, while China is still well behind them in per capita gross domestic product (GDP) terms.

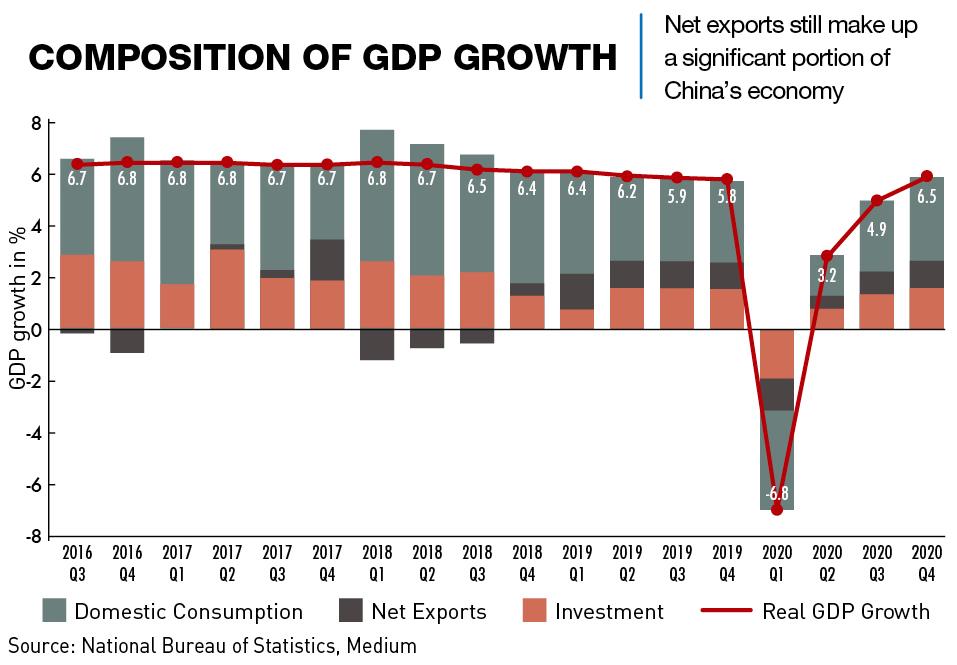

Despite that, the switch is underway. Domestic consumption has been the fastest-growing part of the economy for the last eight years and accounted for 60% of GDP growth in 2019. Retail sales have also increased more than 200% in the last decade, putting them almost on par with the US in dollar terms and growing twice as fast.

“China is the world’s best consumption story and Dual Circulation seems designed to support this trend,” says Andy Rothman, investment strategist for investment firm Matthews Asia.

However, Michael Pettis, Professor of Finance at Peking University, says “China can only rely on domestic consumption to drive a much greater share of growth if workers begin to receive a much higher share of what they produce, so the very process of rebalancing must undermine China’s export competitiveness.”

“This means that for ‘internal circulation’ to succeed, “international circulation” must be undermined,” he wrote in the Financial Times. “One cannot boost the other, as Beijing proposes: the shift itself will require a difficult adjustment period.”

What does it mean?

In various mentions of Dual Circulation since May, President Xi has stressed “dual,” saying that “internal circulation” will be supported by “external circulation.” Details remain scant, but China watchers expect to learn more during the annual parliament session in early 2021 when Dual Circulation is expected to be put forward as a key priority of China’s 14th five-year plan.

“The ‘dual’ part is using domestic and international circulation to reinforce each other,” explains Gilliam Collinsworth Hamilton, China Editor at research company Gavekal Dragonomics. “What that means specifically is weaning the country off its vulnerabilities in global economic trade and using the domestic economy, particularly consumption, as a buffer, just in case global headwinds arise, whether in the form of another trade war or pandemic.”

Investing in tech innovation and pushing manufacturing further up the value chain will affect both internal and external circulation, Rothman says. The smaller export portion of the economy is also likely to shift from developed markets, such as Australia, the European Union and the US, toward developing countries.

Again, this is nothing new. China’s total export value to the EU, United Kingdom and US has been falling. Meanwhile Beijing has been the biggest trading partner for ASEAN countries for the past decade, with bilateral trade reaching $292 billion in the first half of 2019. President Xi’s signature Belt and Road Initiative—a $1 trillion transcontinental trade and infrastructure network—is also diversifying the export portfolio away from more developed countries.

“The government likes slogans,” says Rothman. “Sometimes they have political meanings, sometimes they are just designed to reiterate what’s happening. Dual Circulation is an easy way to describe what’s been going on for a long time.”

How will it be achieved?

Efforts to implement Dual Circulation are being made across all areas of the economy. In July, the Ministry of Industry and Information Technology announced the “same standard, same quality” initiative, aimed at boosting domestic consumption of locally-made goods by ensuring the quality matches those exported. More duty-free shopping areas are also opening in a bid to encourage some of the luxury spending the Chinese are famous for overseas to take place at home.

Meanwhile, government financing and private support is pouring into industries seen as too reliant on imports. Banking and insurance regulators put out a notice in March encouraging banks to lend to China’s “core enterprises,” an effort to accelerate research and development into substitutes for imported components. Energy, pharmaceutical supplies and technology are likely to be the focus of investment, according to the Economist Intelligence Unit (EIU). In the tech field alone, the government has released a multi-billion-dollar fund and 10-year tax exemptions for companies developing domestic alternatives to integrated circuits.

“We believe that under Dual Circulation, reducing these vulnerabilities and fortifying self-reliance in production and distribution will be the priority even if it results in some economic inefficiencies,” says EIU principal China economist Yue Su.

But the building of domestic consumption and supply chains does not appear to be a simple policy of autarky and isolation. Beijing is still encouraging foreign investment, having released guidelines in August on how to streamline regulations for international businesses. Shutting off exports would also be counterproductive given how well Chinese manufacturing performed in the pandemic. Exports rose almost 10% to an all-time high of $239.8 billion in September, buoyed by global demand for medical supplies and personal protective equipment (PPE).

“A great deal of the economy is still dependent on global trade,” says Collinsworth Hamilton from Gavekal. “China’s really trying to have its cake and eat it to gain more control over its long-term growth without losing its position as a central manufacturing hub.”

Whether Dual Circulation is a relabeling of older policies or not, most analysts think it will make life harder for some foreign companies doing business in China. Domestic firms are not only being prioritized and receiving investment, but are also likely to be more adept at executing according to the needs and preferences of domestic consumers. Foreign companies may need to localize operations, invest more in the business ecosystem and align carefully with government policies to compete effectively.

Those that find themselves in the right sector at the right time, however, will still reap rewards. General Motors, which teamed up with SAIC Motor in 1997, has sold more cars in China than in the US for each of the past eight years, while Nike posted 22 consecutive quarters of double-digit revenue growth in China before COVID-19 took hold.

“The rebalancing of the economy toward domestic demand has already turned China into the world’s best consumer store,” says Rothman. “As a result, many foreign companies are making a lot of money selling a lot of stuff to consumers and that’s going to continue.”

Will it work?

Both risk and opportunity will come together with changes in China’s economic policy. Despite the best efforts to boost domestic consumption over the past decade, private consumption as a share of GDP has only increased slightly. As measures have focused on subsidies for consumer-facing industries and incentives for shoppers to make planned purchases earlier, it is unlikely most Chinese, known to be steadfast savers, are going to empty their coffers with gusto, especially after the hit the economy took over the last year.

The EIU is also doubtful about the country’s ability to compete with other global players when it comes to semiconductor design. And while China may reduce imports in the low and mid-range chip sector, a whole new ecosystem will need to develop before manufacturers have workable replacements for the most sophisticated foreign chips. Finally, placing resilience above productivity will come at a cost.

“The new growth model will reduce productivity, thus having an impact on income levels, which will also risk household debt sustainability if wages cannot compete with borrowing cost,” says Yue Su.

“Past growth has depended heavily on the current distortions in income distribution. The transformation to a new model will almost certainly require a difficult adjustment period,” writes Pettis. “For Dual Circulation to work, internal circulation can only come at the expense of international circulation and as this happens, wealth—and with it, power—must be shifted from today’s elites to ordinary households.”

However, according to an October report by Japanese financial holding company Nomura, directing funds to high-end manufacturing could boost productivity and increase growth potential, with China achieving economies of scale in many sectors thanks to its huge population of consumers. This will also enhance commercial opportunities and jobs in key sectors, again helping to boost consumer spending.

“This has been going on for years,” says Stevenson-Yang. “It tends to kill innovation, but if your goal is to spend less on foreign exchange and make more stuff yourself, it tends to be pretty effective.”

Enjoying what you’re reading?

Article Subscribe (1)

CKGSB Report

Related Articles

Our Programs

Scaling Innovation: AI and Digital Strategies for Business Transformation

Global Unicorn Program Series

In partnership with Columbia Engineering

This program is designed to equip senior executives with the strategic insights and tools necessary to lead in this transformative era.

LocationNew York, USA

Date27 Sep - 02 Oct, 2026

LanguageEnglish

Emerging Tech Management Week: Silicon Valley

Global Unicorn Program Series

In partnership with UC Berkeley College of Engineering

This program equips participants with proven strategies, cutting-edge research, and the best-in-class advice to fuel innovation, seize emerging tech developments, and catalyse transformation within your organization.

LocationUC Berkeley

Date01 - 06 Nov, 2026

LanguageEnglish

Asia Start (15th Edition): AI + Digital China Expedition

Asia Start provides entrepreneurs and executives with unparalleled access to Asia’s dynamic digital economy and its business ecosystems, offering the latest trends and insights, strategies, and connections to overcome challenges and unlock future growth for your business in Asia and beyond.

LocationChina (Beijing, Shanghai, Hangzhou & optional Shenzhen)

DateNovember 2-7, 2026

LanguageEnglish

Intelligent China: AI, EVs & Advanced Manufacturing

Participants may join the full 12-day journey or select individual modules based on their interests and priorities.

LocationBeijing, Shanghai & Hangzhou

Date12 Days

LanguageEnglish

Stanford & Silicon Valley Immersion Program

Global Unicorn Program Series

In partnership with Stanford Engineering Center for Global & Online Education

This CKGSB program equips entrepreneurs, intrapreneurs and key stakeholders with the tools, insights, and skills necessary to lead a new generation of unicorn companies.

LocationStanford University Campus,

California, United States

Date06 - 11 Dec, 2026

LanguageEnglish with Chinese Translation