South-East Asia has become the latest battleground for e-commerce companies. Can China’s tech giants win by proxy?

In many parts of the world, the idea of online shopping and Amazon go hand in hand, but in South-East Asia, it is players with Chinese involvement that have taken the lead. It was Alibaba that created Singles Day in its home market a decade ago, taking consumerism in China to new heights. In 2019, Alibaba’s Singles Day sales reached an unprecedented $38.4 billion, well above 2018’s $30.7 billion.In the first hour of the November 11 24-hour online shopping frenzy known as Singles Day, South-East Asia’s top e-commerce platform Lazada received a record 3 million orders—double the previous year’s number. The orders flooded in from Indonesia, Malaysia, Vietnam and elsewhere, in what is easily the most effective sales event in the region. But for Lazada, its focus on Singles Day may also have something to do with the 83% ownership stake that Chinese e-commerce titan Alibaba holds in it.

China’s e-commerce market remains robust, but the market has matured, causing Alibaba and its competitors to look overseas in pursuit of new avenues of growth. Neighboring ASEAN countries, which include Indonesia, Malaysia, Philippines, Singapore, Thailand and Vietnam to the south, were an obvious and promising target.

Outgrowing the pond

“The China [e-commerce] market is saturated,” says Ben Cavender, managing director of the Shanghai-based consultancy China Market Research Group (CMR). South-East Asia, on the other hand, is on the cusp of large-scale expansion. The region’s “large consumer classes and mobile-savvy users” make it a logical choice for China’s internet giants as they seek to build global e-commerce businesses, he adds.

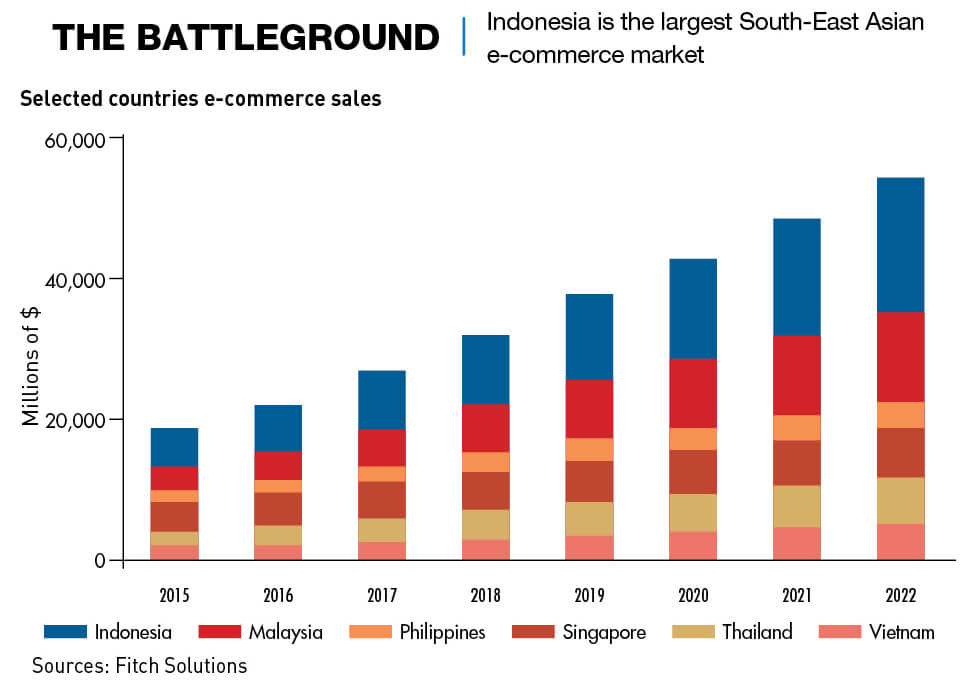

Forrester Research, in a report titled Online Retail Forecast, 2018 To 2023 Southeast Asia, forecasted that South-East Asia’s online retail market will reach $53 billion by 2023, up from $19 billion in 2018. The most important market is Indonesia, South-East Asia’s largest nation by size of economy, land area and population (272 million). Some 90% of the country’s internet users between the ages of 16 and 64 report that they already buy products and services online, according to Hootsuite, a social media management platform. But growth potential is still massive: The average e-commerce user in Indonesia spent just $89 online last year, statista found, compared to $858 in China and $1,800 in the United States.

“What’s important to remember about Indonesia is not just that it’s big, but that it’s bigger than the next three most populous South-East Asian countries combined,” says Kay-Mok Ku, a managing partner at Gobi Partners, a Singapore-based venture-capital firm.

Those three countries are the Philippines, Vietnam and Thailand, which have populations of 105 million, 91 million and 69 million respectively. Along with Indonesia, they comprise South-East Asia’s paramount e-commerce markets.

Three major Chinese players

Compared to China’s e-commerce market, South-East Asia is more diverse with fewer restrictions on foreign investment. It’s a new ballgame for China’s internet giants.

“South-East Asia is an emerging region but also a very open market,” says Jessica Liu, a partner at Taipei-based AppWorks, one of Asia’s largest accelerators. “It comes back to understanding that no matter if a company is Chinese or from another country, Greater South-East Asia is still a level playing field for all companies.”

And while there are numerous e-commerce players competing for the South-East Asian market, the leaders in the game are Alibaba, Tencent and JD.com (although it should be remembered that Tencent has a 20% stake in JD.com), all of which are China-based.

Alibaba’s South-East Asian strategy

Alibaba has been among the most aggressive foreign e-commerce firms in South-East Asia, and it has a commanding stake in several of the region’s largest local online marketplaces. It initially gained control of Lazada in 2016 with a $1 billion investment, which at the time was its largest investment outside of China. In 2017, it increased its stake in Lazada from 51% to 83%.

Following up on its investment in Lazada, Alibaba led funding rounds of $1.1 billion in 2017 and 2018 into the major Indonesian e-commerce player Tokopedia, giving the Chinese company a foothold in the region’s largest market. Tokopedia was Indonesia’s most-visited e-commerce site from the second quarter of 2018 through the quarter ended June 2019 with 140.4 million visits, according to online shopping aggregator and e-commerce data provider iPrice.

Compared to Tencent and JD.com, Alibaba appears more intent on replicating its China digital services ecosystem with e-commerce at its core in South-East Asia. “It (Alibaba) is bringing a proven model which is ultimately bringing China’s retail to the South-East Asian market,” says Declan Kearney, the APAC Managing Director of Edge by Ascential, a digital retail insights and consulting provider.

The model has worked well for Alibaba in China, where it understands consumer behavior and can count on regulatory support. Alibaba has built a giant digital bazaar with Taobao and Tmall and provides an easy online payment option, the e-wallet application Alipay, in a country where credit cards have never been widely used. Later, armed with all the user data gleaned from its online marketplaces, Alibaba expanded into online lending with MyBank.

Tencent’s South-East Asian strategy

Alibaba’s biggest competitor, Tencent, is taking a different approach to South-East Asia. With a 40% stake in e-commerce and game publisher Sea, Tencent is the biggest shareholder in the Nasdaq-listed parent company of the Singaporean online shopping site Shopee.

The investment in Sea is strategic for Tencent as it gives the Chinese company a regional foothold in both online shopping and gaming—the latter being Tencent’s largest source of revenue.

Sea is ASEAN’s biggest gaming platform with roughly 161 million active users each quarter. Under the deal, Sea has the right of first refusal to publish Tencent’s games in Indonesia, Malaysia, Singapore, Taiwan, Thailand and the Philippines.

JD.com’s South-East Asian strategy

Meanwhile, JD.com has invested in the Vietnamese e-commerce site Tiki.vn, Indonesian travel-booking platform Traveloka, Thai online fashion site Pomelo, and Thailand’s Central Group, a major real estate, retail and hospitality conglomerate. The $500 million deal between JD.com and Central Group involves financial technology (fintech) as well as online shopping.

“Tencent is less focused on e-commerce than Alibaba—they just want to capture digital services, whatever that may be,” CMR’s Cavender says.

Will These Different Strategies Work?

“In the initial stage, Alibaba can take time to understand how the local e-commerce platforms operate and further improve its control over them. Later, it has the option to increase or reduce its investment,” says Rose Chang, an e-commerce industry analyst at the Taipei-based Market Intelligence & Consulting Institute.

Mobile payments are starting to gain traction in South-East Asia, but the economy is still very cash-focused, far more so than in China. “In Indonesia, not everyone has a credit card or even a bank account, so companies like Lazada have localized by allowing cash on delivery,” says APAC’s Kearney. “We see South-East Asia rapidly gaining on the advancements of China within the next few years.”

Alibaba also faces competition in South-East Asia on a level it has never experienced in China. In contrast to South-East Asian countries, “the regulator acts as a promoter in China,” says Gobi Ventures’ Ku. “It takes a national champion approach.”

Indeed, as Alibaba has become dominant in e-commerce, it has positioned itself to also become one of China’s leading internet finance platforms. Chinese regulators granted MyBank a coveted online lending license in 2015. The only other company that has so far received one is Tencent-backed WeBank. But these financial operations are effectively confined to the China market, for now.

Alibaba doesn’t have an obvious path to fintech dominance in South-East Asia,” says Zennon Kapron, director of Singapore-based Kapronasia, a research firm and consultancy focused on the financial services sector. He notes that ASEAN’s digital payments space is highly fragmented, with a huge array of competitors, from traditional credit cards to the fintech arms of ride-hailing giants Grab and Go-Jek to the dedicated digital wallets of different e-commerce platforms, like ShopeePay.

Some analysts say that Alibaba could benefit by developing better local strategies, given the uniqueness of each ASEAN country’s market. “Investing the time and resources needed to localize will be key (to success),” says Kearney.

Liu contrasts Tencent’s approach to South-East Asia e-commerce favorably with Alibaba’s. “The typical Chinese e-commerce story [Alibaba’s] is about taking a proven model in China and going outside of the China market, and executing to the core strengths of the company,” she says. “But Tencent is a totally different story. They are partnering with local companies overseas and using their investment arm to empower the local ecosystem.”

When looking at JD.com, Baseer Ahmad Siddiqui, a Kuala Lumpur-based ASEAN software analyst for market researcher IDC, believes that JD Central has the potential to dominate if it lives up to its commitment to provide consumer “peace of mind” with 100% authentic goods and offering them a unique customer experience.

“JD Central may do acquisitions of smaller marketplaces to expedite their customer acquisition, as challenging Lazada’s position as a market leader needs a very effective market penetration and customer retention strategy.”

Kok Hoi Wong, the chief investment officer for APS Asset Management Pte in Singapore, disagrees, saying the company needs to fine-tune its strategy in its home market before attempting to lead in markets abroad. “JD must get its act right in China, turn it around and make it profitable before it expands internationally,” said Wong. Brutal competition among hundreds of e-commerce players means business is tough for all online retailers and “we will see more blood before we see more profit.”

International competitors

A wide variety of other international e-commerce firms are vying for market share across South-East Asia too. These include South Korea’s Gmarket and SK Planet, as well as Amazon and eBay from the US. But none come close to the dominance that Chinese e-commerce players have in the region.

E-commerce is fiercely competitive in South-East Asia, and Amazon is struggling to compete in a crowded market. Despite positive media attention around the implementation of Amazon Prime in Singapore, Amazon’s presence in South-East Asia lags far behind its Chinese competitors. Its best markets are the Philippines and Thailand, where it comes in as the fourth and fifth most popular e-commerce platforms respectively. Elsewhere, Amazon’s footprint is almost invisible—it is ranked seventh in Vietnam, eighth in Singapore, ninth in Malaysia and 10th in Indonesia.

Should Amazon step up its presence in South-East Asia, as some analysts expect it will, then competition would intensify. “Amazon has the capability and proven experience of opening up markets,” says AppWorks’ Liu. “When they go after a market—India for instance—they perform with a high degree of confidence and commitment. They also have extensive operational experience overseas compared to other platforms.”

Fragmented victory

Unlike in China, where their respective platforms have gone head to head, Alibaba and Tencent battle for e-commerce market share across South-East Asia only indirectly, primarily through strategic acquisitions. The crossover in ownership among some of these firms also causes some unusual market dynamics. For instance, Lazada and Tokopedia, both backed by Alibaba, are direct competitors in Indonesia.

One South-East Asia-based investor, who spoke to CKGSB Knowledge on condition of anonymity, suggests that Alibaba might be interested in taking majority ownership of Tokopedia in the event that the current majority shareholder, Japan’s Softbank, is forced to divest some of its shares—a possibility if the company needs cash. “Alibaba might be able to take over Tokopedia for a good price,” the person says.

Softbank posted a massive $6.5 billion loss in the third quarter of 2019 following weak performances by ride-hailing giant Uber and office-sharing startup WeWork, two of its portfolio companies. It was Softbank’s first quarterly loss in 14 years.

If Alibaba assumed control of Tokopedia, it would have a stronger position in the Indonesian e-commerce market and could focus Lazada’s resources elsewhere in the region, where it is performing better. Lazada was the No. 4 e-commerce firm in Indonesia behind Tokopedia, Shopee and Bukalapak in the first quarter of the year, according to iPrice.

Tencent-backed Shopee has emerged as Lazada’s main regional rival. In the quarter ended March 2019, Shopee became ASEAN’s most visited e-commerce platform as website and app traffic increased 5% to 184.4 million visits from the fourth quarter of 2018, iPrice found. During that period, Shopee was the No. 1 e-online marketplace in Vietnam and second in Malaysia, the Philippines and Thailand.

Ultimately, strategic acquisitions give China’s e-commerce giants a strong foothold in ASEAN, but it will be difficult for them to dominate all the major markets. Tailoring business strategies for individual ASEAN markets will be essential as consumer tastes differ greatly from China and there is much diversity within the region too.

Gobi Partners’ Ku believe that the experience of Japanese companies expanding internationally in fields including auto production and electronics manufacturing in the late 20th century, could be instructive for China’s e-commerce giants in South-East Asia, “The Japanese have gone through this,” he says. “When they first started going overseas, they brought all of their systems from Japan, and they found that what worked in Japan, didn’t necessarily work elsewhere—so they adapted.”

Enjoying what you’re reading?

Article Subscribe (1)

CKGSB Report

Our Programs

Scaling Innovation: AI and Digital Strategies for Business Transformation

Global Unicorn Program Series

In partnership with Columbia Engineering

This program is designed to equip senior executives with the strategic insights and tools necessary to lead in this transformative era.

LocationNew York, USA

Date27 Sep - 02 Oct, 2026

LanguageEnglish

Emerging Tech Management Week: Silicon Valley

Global Unicorn Program Series

In partnership with UC Berkeley College of Engineering

This program equips participants with proven strategies, cutting-edge research, and the best-in-class advice to fuel innovation, seize emerging tech developments, and catalyse transformation within your organization.

LocationUC Berkeley

Date01 - 06 Nov, 2026

LanguageEnglish

Asia Start (15th Edition): AI + Digital China Expedition

Asia Start provides entrepreneurs and executives with unparalleled access to Asia’s dynamic digital economy and its business ecosystems, offering the latest trends and insights, strategies, and connections to overcome challenges and unlock future growth for your business in Asia and beyond.

LocationChina (Beijing, Shanghai, Hangzhou & optional Shenzhen)

DateNovember 2-7, 2026

LanguageEnglish

Intelligent China: AI, EVs & Advanced Manufacturing

Participants may join the full 12-day journey or select individual modules based on their interests and priorities.

LocationBeijing, Shanghai & Hangzhou

Date12 Days

LanguageEnglish

Stanford & Silicon Valley Immersion Program

Global Unicorn Program Series

In partnership with Stanford Engineering Center for Global & Online Education

This CKGSB program equips entrepreneurs, intrapreneurs and key stakeholders with the tools, insights, and skills necessary to lead a new generation of unicorn companies.

LocationStanford University Campus,

California, United States

Date06 - 11 Dec, 2026

LanguageEnglish with Chinese Translation