A new phase: China’s Belt and Road sees reinvigoration

February 26, 2026

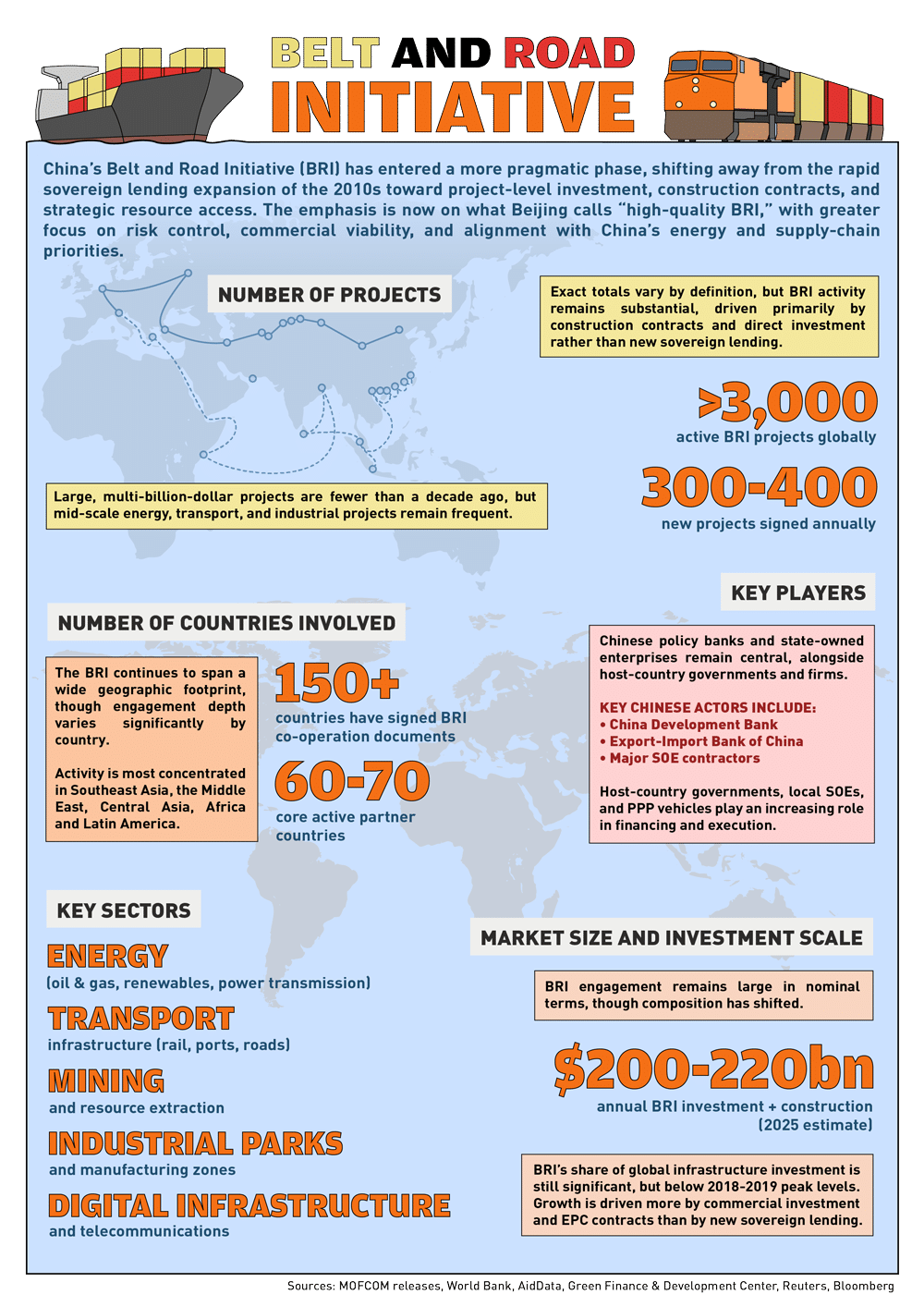

China’s Belt and Road Initiative is entering a new phase, with a recent bump in infrastructure and construction spending signaling Beijing’s intent to reassert leadership in global development

The Torugart Pass has been used since antiquity to cross the Tian Shan mountain range that straddles present-day China and Central Asia. What was once a favoured junction for merchant caravans plying the ancient Silk Road is now set to see renewed relevance as a stop along the China-Kyrgyzstan-Uzbekistan (CKU) Railway, a landmark $4.7 billion project of the Belt and Road Initiative (BRI) that will offer a shorter, more cost-effective overland route for freight transport between China and Europe via Central Asia, while serving as a gateway to Chinese coastal ports for Kyrgyzstan and Uzbekistan.

Multibillion-dollar megaprojects like the CKU Railway were once the fundamentals of the BRI, launched in 2013 as a cornerstone of President Xi Jinping’s policy to boost China’s global economic and political influence through massive infrastructure investments across Asia, Europe, Africa, and beyond. And while BRI engagement in terms of contractual and investment value soared to a record high of $213.5 billion in 2025, the rail link and other BRI projects are taking shape amid a different backdrop than a decade ago, with China facing both slower economic growth and greater geopolitical uncertainty.

The railway and other ambitious developments approved last year represent a return to larger infrastructure projects for the BRI, following a trend of “small but beautiful” initiatives over the past several years.

“What initially seemed like an airy vision statement by a fresh new Chinese leader seeking a way to imprint himself has evolved into something far more concrete and impactful,” says John Calabrese, assistant professor at the School of Public Affairs at American University in Washington DC.

“The BRI graduated from a mere slogan to a global framework for investment, connectivity, and influence,” he says. “Its trajectory is closely intertwined with Xi’s consolidation of power and with China’s own ascent in global status, ambition and influence.”

Banking on the Belt and Road

Xi has used the BRI to deepen China’s economic influence and trade ties with 150 countries, particularly in the developing world. By the end of 2025, BRI engagement reached a cumulative $1.39 trillion, equivalent to the size of a top-20 economy such as Saudi Arabia. And of the $213.5 billion in BRI engagement last year, $128.4 billion went on construction contracts and $85.2 billion to investments. Some $93.9 billion was related to energy, with the lion’s share allocated to oil and gas developments.

The strategy that began life as a vague suggestion from Xi to revive the Silk Road has notched up some tangible achievements—it has facilitated the construction of thousands of kilometers of railways and roads connecting China to Central Asia, Europe, and Southeast Asia; established ports, logistics hubs, and industrial parks across Asia, Africa, and the Middle East; and invested in energy, digital, and telecommunications infrastructure around the world.

“It is worth noting that much of this infrastructure addressed pressing needs in the Global South, and that these projects were largely welcomed—or even actively sought—by partner countries, though not all were entirely successful and some failed or were problematic,” says Calabrese.

Beyond physical infrastructure, the initiative has strengthened trade links, deepened financial connectivity through banks and currency arrangements, and expanded China’s diplomatic and strategic footprint. “Despite its challenges and criticisms, the BRI shows that China has devised a lasting, evolving, and important way of engaging with the world,” says Calabrese.

China has also harnessed the BRI as a vehicle for its plans to remake the rules-based order. The Chinese government has always sought to use the scheme to enhance its own image and boost its weight in the world. Increasingly, however, it is also being used to rally the global south around China’s own model of development.

One of the attractions of the BRI for many countries in contrast to Western development funds is that investments tend to include fewer extraneous commitments and there is generally less oversight into everyday workings of the project, such as timetables or actual usage of funds.

Chinese construction companies and financiers helped propel the BRI in its earliest years, with a particular focus on major infrastructure projects in emerging markets, such as the Addis Ababa-Djibouti Railway, the Jakarta-Bandung Railway, and sections of the Pan-Asian Railway, according to Chim Lee, a senior analyst in Beijing at the Economist Intelligence Unit (EIU) who covers the BRI.

“Over time, the focus on infrastructure and development financing has been balanced by private Chinese firms—especially manufacturers—actively investing overseas,” says Lee, who explains that investments have tended to follow four logics: market expansion, supply-chain development, securing resources, and/or technology and innovation.

“Amid intense competition at home and rising protectionism across markets, Chinese firms are further incentivized to localize production in emerging markets,” says Lee. “This has been particularly evident in the automotive sector in countries like Thailand and Hungary.”

While there have been positive outcomes from the BRI, for both China and the countries that have received BRI-related spending, the initiative has not been without its controversies. These range from small, project-related issues to larger concerns regarding China’s approach to deal-making or geopolitical impacts.

At a project level, there have been several criticisms of built infrastructure, either being left incomplete or failing to meet specifications, and in some cases falling apart after only a short period of use.

China has also been accused of undertaking ‘debt-trap diplomacy’ by financing projects with a low level of commercial viability, something which Beijing has always denied, and several scholars have also called into question. Dozens of the world’s poorest and most vulnerable countries were scheduled last year to spend a record $21.62 billion on servicing Chinese debt, a “tidal wave” of loan repayments and interest costs mostly related to lending under the BRI.

Nowhere is China’s swing from bilateral banker to debt collector more apparent than in Africa, where countries that received BRI funding now spend more to repay loans than they receive in new Chinese financing. This reversal has led to trouble for countries elsewhere, such as Laos, where a hydropower investment binge in the mid-2010s, fuelled by China’s outsized lending, helped trap the debt-stricken nation in a severe economic crisis that will likely require cooperation from Beijing to resolve.

Chinese enthusiasm for lending to the developing world has also raised questions about governance, given that many of the governments in recipient countries are associated with notable levels of corruption. More than one-third of BRI infrastructure projects had encountered implementation problems that include corruption scandals, according to an American study in 2021.

Beauty makeover

The criticism, combined with a tighter macroeconomic environment in China, led the BRI to pivot toward “small but beautiful” programs with higher standards and better returns—a recalibration of the BRI first described by Xi at a BRI symposium in 2021. The evolution saw a shift away from traditional heavy infrastructure toward renewables, power transmission, telecoms, data centers, electric vehicle supply chains and light manufacturing—sectors that tend to involve smaller ticket sizes, faster payback periods and greater scope for private investment than transport megaprojects.

The small but beautiful adjustment also reflected lessons learnt by China after it was stung by the criticism. Beijing reduced the BRI’s political exposure by moving away from headline-grabbing, debt-heavy megaprojects and toward smaller, commercially viable investments, using more shared financing and aligning projects more closely with host-country priorities. This has blunted Western criticism over debt and transparency while giving China more room to adjust, scale back, or walk away when political conditions shift.

“Lesson number one from the first BRI wave relates to risk and backlash. Scaling projects down reduces exposure while making them easier to adjust, pause, or exit if conditions deteriorate,” says Calabrese. “Lesson number two is that host country preferences and politics matter—smaller projects with private participation are easier to justify politically and fiscally.”

Back to big

That said, last year’s record contracting and investment activity under the BRI, as well as the green light for several multibillion-dollar projects, suggests big infrastructure is back in vogue in Beijing. “The ‘small but beautiful’ projects in the BRI propagated through official channels during COVID should be seen as bygone,” says Christoph Nedopil Wang, director of the Griffith Asia Institute and economics professor at Griffith University. “Now, we don’t have large, small… we have all types of projects. The sky’s the limit.”

Underpinning this notion is that China made meaningful progress in 2025 on a handful of BRI megaprojects—namely the Mubarak Al-Kabeer Port in Kuwait, China-Kyrgyzstan-Uzbekistan Railway, and China-Laos Economic Corridor. Also catching the eye were the $20 billion Ogidigben Gas Revolution Park in Nigeria and a $1.6 billion engagement by Harbin Electric in Saudi Arabia for a natural gas-fired power plant. “These types of projects, on their current scale, we have not seen many since the early years of the BRI,” says Calabrese.

“Strategic geography matters,” he says. “Each of the projects… occupies a key node in China’s overland and maritime connectivity ambitions. For example, the CKU Railway advances Beijing’s effort to diversify westward corridors that bypass Russia while deepening Central Asia’s integration with Chinese supply chains.”

The BRI has been framed since its launch in 2013 as part of China’s multi-pronged challenge to the US-led geopolitical order. And while Beijing has worked to shore up the credibility and durability of the BRI, the job of promoting the scheme has been made easier by Washington’s coercive approach to international trade and foreign policy under the Trump administration. “What we’re seeing right now is a doubling-down on engagement in countries of the BRI and also in countries that are aligned with China outside of the BRI, like Brazil,” says Wang.

Hindrances to BRI

While the assumption is that a more capricious US could send countries running to the BRI, this may not necessarily be the case. The downfall of Venezuela’s former president Nicolás Maduro in January marks a geopolitical test for China that will have downsides for the BRI, according to the EIU’s Lee.

“The development bodes ill for the BRI in Latin America, which we expect to experience a tough 2026 as Trump shifts his attention to the western hemisphere,” says Lee. “Many countries in the region are likely to become less receptive to Chinese involvement in their infrastructure, energy, and mining projects.”

In truth, BRI engagement in Latin America has been minimal, standing at just $4 billion in 2025. But a more muscular and unpredictable US foreign policy adds to the list of pitfalls that could hinder the BRI’s expansion.

A more sluggish and complicated macroeconomic environment compared with 2013 could tap the brakes on some of Beijing’s grandest ambitions for the BRI. Slower growth, local government debt pressures, a stressed property sector, and greater scrutiny of overseas lending have limited the appetite of policy banks for long-term, sovereign-backed megaprojects.

But rather than forcing a retreat, weaker growth will “likely reinforce trends already visible, namely tighter selectivity, smaller project sizes, and greater emphasis on risk control,” says Calabrese.

Other additional challenges that China might find itself facing in the years ahead include the fact that Beijing remains tied down by early BRI loans in debt-distressed countries, with restructurings absorbing capital and political attention that would otherwise support new projects. Next are unpredictable host-country developments with which China will have to contend, whether in the form of leadership turnover or fiscal stress.

Then there is the emergence of heavyweight alternatives to the BRI— for instance, the EU has mobilized €300 billion ($355 billion) for its Global Gateway infrastructure initiative to spend on digital, climate and energy, transport, health, and education projects worldwide.

Here to stay

It is unclear if last year’s pick-up in BRI funding for large-scale developments heralds a return to the megaproject era, as views are split on whether engagement will maintain momentum. Wang says he expects Chinese BRI engagement to ease this year with fewer major deals, while the EIU anticipates headline figures in aggregate to rise but fewer megaprojects. Going forward, the BRI projects are likely to be smaller in scale but more strategic in purpose—focusing on key corridors and sectors, financed through blended models, and embedded even more deeply in host-country plans.

A more nuanced, ‘dual-track’ approach is likely in the form of some limited megaprojects and others that are commercially oriented, reflecting considerations over financial returns and a desire for smaller-scale, higher-return and de-risked developments, according to EIU’s Lee.

At the same time, China will want to take advantage of the Trump administration’s disengagement by showing a continued willingness to finance large projects that carry geopolitical significance, such as the CKU Railway. “The Chinese are extremely flexible and adaptable to new circumstances,” says Wang. “That’s one strength of the Chinese that will not go away, so even if the world becomes more fractured, I think they will find a way to capitalize.”

Enjoying what you’re reading?

CKGSB Report

Related Articles

Our Programs

Opportunities in the Disruption of Traditional Industries

In partnership with The University of Sydney

Global Unicorn Program Series

The Global Unicorn Program in Disruption of Traditional Industries – presented jointly by CKGSB and University of Sydney – will emphasize Australia’s distinctive contributions.

LocationSydney, Australia

Date24 - 27 Feb, 2026

LanguageEnglish

Emerging Markets: Innovation and Scaling for Exponential Growth

Global Unicorn Program Series

A joint program by Cheung Kong Graduate School of Business and The South Africa Chamber of Commerce and Industry

LocationJohannesburg, South Africa

Date20 - 23 Apr, 2026

LanguageEnglish

Asia Start: AI + Digital China Expedition

Asia Start provides entrepreneurs and executives with unparalleled access to Asia’s dynamic digital economy and its business ecosystems, offering the latest trends and insights, strategies, and connections to overcome challenges and unlock future growth for your business in Asia and beyond.

LocationChina (Shanghai, Hangzhou, Shenzhen)

Date11 - 14 May, 2026

LanguageEnglish

Scaling Innovation: AI and Digital Strategies for Business Transformation

In partnership with Columbia Engineering

Global Unicorn Program Series

This program is designed to equip senior executives with the strategic insights and tools necessary to lead in this transformative era.

LocationNew York, USA

Date27 Sep - 02 Oct, 2026

LanguageEnglish

Emerging Tech Management Week: Silicon Valley

In partnership with UC Berkeley College of Engineering

Global Unicorn Program Series

This program equips participants with proven strategies, cutting-edge research, and the best-in-class advice to fuel innovation, seize emerging tech developments, and catalyse transformation within your organization.

LocationUC Berkeley

Date01 - 06 Nov, 2026

LanguageEnglish

Stanford & Silicon Valley Immersion Program

In partnership with Stanford Engineering Center for Global & Online Education

Global Unicorn Program Series

This CKGSB program equips entrepreneurs, intrapreneurs and key stakeholders with the tools, insights, and skills necessary to lead a new generation of unicorn companies.

LocationStanford University Campus,

California, United States

Date06 - 11 Dec, 2026

LanguageEnglish with Chinese Translation