Multinationals in China are coming under increased scrutiny due to allegations of tax evasion.

In November 2014, shockwaves were felt when the Chinese government handed out an RMB 840 million ($140 million) fine to a US technology group over alleged tax evasion. The company, identified by Chinese news agency Xinhua as ‘M’, was widely believed to be Seattle-based computer giant Microsoft due to the background information the news agency supplied on the company. Xinhua’s report alleged ‘M’ had admitted to booking profits in offshore tax havens, reporting a loss in China, thereby avoiding tax. It suggested the company had admitted to tax ‘evasion’.

Although never confirmed, in a media statement at the time Microsoft said the US and Chinese tax authorities had signed an agreement in 2012, an “acknowledgment by both countries that Microsoft’s profits are subject to the appropriate tax in China”.

This incident has been interpreted as the start of a crackdown on certain tax structures by the Chinese government. Xinhua said ‘M’ was reporting losses averaging 18% over the past six years, while paying more than half of its profits to its US headquarters as development funds and franchise fees.

This practice, known as transfer pricing, is not uncommon among international companies, and is not a challenge exclusive to Chinese tax authorities. Multinationals can transfer profits to subsidiaries or separate arms of their company in another tax jurisdiction, which can be claimed as management fees, expenses or similar. This means a lower amount of profit is declared in the original tax jurisdiction.

“All countries face tax enforcement problems when dealing with multinationals, given the ease with which multinationals can shift profits across borders through transfer pricing and other means,” says Roger Gordon, economics professor at the University of California, San Diego. “There is no ‘right’ measure for these transfer prices, making enforcement decisions rather arbitrary, and if you want, political.”

Leveraging the Loopholes

Tax experts point out that although the word ‘evasion’ is frequently used when discussing transfer pricing, the practice is not illegal. It is generally considered to be ‘avoidance’—a legal use of loopholes, or incoherent laws to eliminate tax burdens. But for others this practice is simply unfair, and it has been a political hotspot in many nations over the last few years. Multinationals such as Starbucks have faced media hostility and government probes, particularly in the US and UK. In many ways, the Microsoft case simply reflects a collective global mood.

“What would have happened in [the ‘M’ case] is that China would have been perhaps unhappy about the cost allocation left to China,” explains Chas Roy-Chowdhury, Head of Taxation at the Association of Chartered Certified Accountants. “It doesn’t mean to say it’s anything illegal, just the nature of transfer pricing.”

“One of those problems around transfer pricing is that information where you have got transactions going on between related companies is very onerous, very difficult to obtain,” he continues. “There may be a number of shaded areas of grey.”

With these grey areas, it is difficult to accurately calculate how much tax is being “lost” in China. Estimates from the Tax Justice Network suggest China may be losing up to $134 billion annually in tax revenue, although most developed economies struggle to accurately calculate their “tax gap”. The UK probably comes closest, projecting that £34 billion ($51 billion) is the difference between what is and should be collected. That UK figure includes both evasion and avoidance, but also fraud and errors made by taxpayers or by the tax authorities.

“Chinese tax rates are roughly comparable to those in the US,” says Gordon, and so without evasion, tax revenue as a percentage of GDP should be roughly the same. Prior to around 2000, this was around half the US’s, but it has been growing steadily ever since, “suggesting a steadily declining amount of evasion from domestic firms.”

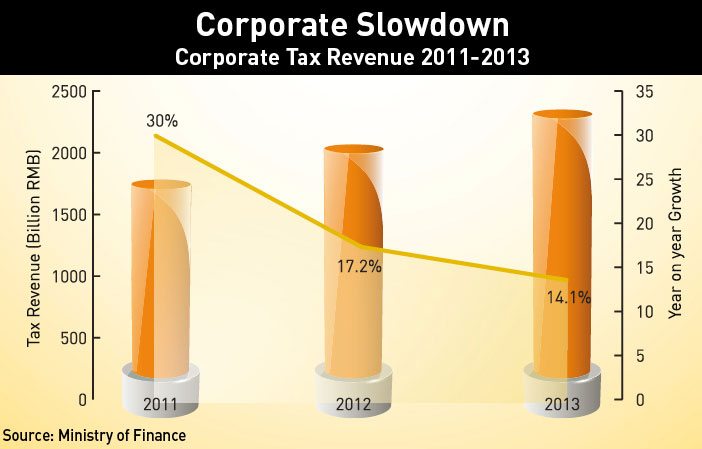

The most recent figures from the State Administration of Taxation (SAT) showed that RMB 7,795 billion ($1,247 billion) in tax revenue was collected in the first three quarters of 2014, which is a 7.4% annual increase on the same period a year before, and matches economic growth.

“With the development of IT technology and strengthened cooperation between tax authorities and other government administration bodies, China’s capability in tax collection is actually improving rapidly,” says Matthew Mui, tax partner at PwC China.

And with its massive population, China needs its income to be steady. Government income as a share of GDP saw a huge decline between 1978 and 1998 as the economy changed, going from 32% to 12%, meaning tax is an even more important source of income. Yet China Daily reported that small firms been exempt from a total of RMB 37.1 billion ($5.95 billion) of taxes in the first nine months of 2014. These are popular decisions for businesses, but mean tax authorities need to shift focus to other areas to make sure tax income stays steady.

Local government revenue is also being hit by a slowdown in the property markets. Land sales in 2013 were equivalent to about 61% of local-government revenue, according to figures from China’s Ministry of Land and Resources and the Finance Ministry. Figures compiled by Bloomberg in May 2014 said land sales in 20 major cities fell 5% in March from a year earlier.

One challenge has been improving the enforcement of domestic tax collection, a problem for many years. China’s prevailing cash economy leaves it vulnerable to tax fraud, although the introduction of a lottery system on receipts, where consumers can win up to RMB 5,000, has helped.

The government has been reforming other areas of the tax system, including transforming a less efficient business tax framework into a newer, modern value-added tax (VAT) system. This is more in line with other countries, and has brought more into the tax system.

“As they make the direct tax system more clear and beef up the system for indirect tax, they are encouraging companies to come forward voluntarily because they want to claim back VAT on their indirect tax,” says James Lee, Regional Director for Greater China at the Institute of Chartered Accountants in England and Wales.

With these measures tackling domestic taxpayers, the government is now paying more attention to global matters. Global Financial Integrity estimates that between 2000 and 2011 $3.79 trillion flowed out of China, more than any other developing country.

According to Xinhua, the SAT is now developing a system to track profit indicators of multinational corporations, after revenue recovered from tax-evasion cases rose to RMB 46.9 billion last year from RMB 460 million in 2005. Turning focus to multinationals is both practical and political.

“China raised the corporate tax rate on multinationals operating in China from half the domestic rate up to the full domestic rate a few years ago,” says Gordon. “The favorable treatment in the past was presumably an inducement to bring modern technology to China, facilitating technology transfer to domestic Chinese firms.” But that motivation has been lost as Chinese firms have progressed technologically. “Multinationals instead are now viewed more as competitors… leading to a more hostile environment.”

There are fears that an increase in tax regulation could go the same way as the monopoly and antitrust campaign last year, which was widely seen as a crackdown on international companies—an antitrust investigation was even opened into Microsoft’s local business practices last July.

A Global Concern

While targeting international companies can be popular for domestic reasons, as multinationals will no longer be seen to be getting special treatment, China’s driving motivation is as much about international politics.

China is part of the G20 group of nations, which in 2013 asked the Organisation for Economic Cooperation and Development (OECD) to develop a plan to tackle the problems around multinational companies shifting profits between jurisdictions.

The subsequent Base Erosion and Profit Shifting (BEPS) proposals from the OECD include the exchange of information between nations, simultaneous tax examinations and assistance in tax collection.

“Most arrangements or structures identified as eroding tax bases of some tax jurisdictions take advantages of asymmetric features in domestic and international tax rules and are technically legal,” explains Mui. As such, the BEPS Action Plans coordinate tax treaties and domestic tax rules, as well as the practices of multinationals.

China gave the OECD convention a boost when it signed up last August—56 countries have now given their support. At November’s G20 summit, President Xi Jinping made a speech calling for greater global cooperation to clamp down on tax evasion. According to the SAT, this was the first time tax affairs were discussed by a Chinese leader at such a high-profile political event.

“[The] BEPS project is a very good opportunity for China to shift its role from international tax rule follower to an international tax rule participant or maker,” adds Mui.

China has even signed up to global tax law FATCA (the Foreign Account Tax Compliance Act), which requires foreign banks to reveal details about American accounts holders, and reciprocal information about wealthy Chinese in America.

As nations work to secure as much tax income in their own jurisdictions, tax enforcers in China are becoming more proactive.

“In China there are a lot of tax areas where there have been regulations for a long time, but there was a lack of enforcement,” says Lee. “In the meantime companies try to maximize their tax deduction based on conventional interpretation of the regulations. People are doing this as a method of just normal business sense. And if there is no interpretation from the tax authority, then it is very difficult for companies to draw the line over what level of tax to pay.

Lee says that China is reacting to the fact tax authorities in other countries are getting more aggressive, and they stand to lose out if they don’t too. “They fear that if they don’t do a good job at collecting their fair share of tax, multinationals [both foreign and Chinese] will just minimize paying tax in China so they can afford to pay tax elsewhere.”

The changing tax landscape both globally and in China will inevitably have implications for business. According to Mui, they will need to monitor and address tax risks, transactions that might be challenged under BEPS and be aware of regulatory developments. That includes reviewing whether profits left in China are in line with global and domestic tax standards.

And as Chinese regulators get more aggressive, most experts expect there to be future enforcement orders like that handed out to ‘M’. While bringing domestic benefits, some have raised concerns it might prove a disincentive for international companies to operate in China. But the international tax crackdown is also an opportunity for China to show its power on the global stage and expand its international tax collection network. As Mui puts it, “Both the global crackdown and China’s self-motivated efforts are influencing the situation, and mutually influencing each other. China needs to participate in the world, and the world needs China’s participation.”

Enjoying what you’re reading?

CKGSB Report

Related Articles

Our Programs

Global Unicorn Program: Scaling for Success in the Age of AI

In partnership with Stanford Engineering Center for Global & Online Education

Global Unicorn Program Series

This CKGSB program equips entrepreneurs, intrapreneurs and key stakeholders with the tools, insights, and skills necessary to lead a new generation of unicorn companies.

LocationStanford University Campus,

California, United States

Date29 Sep - 03 Oct, 2025

LanguageEnglish with Chinese Translation

Emerging Tech Management Week: Silicon Valley

In partnership with UC Berkeley College of Engineering

Global Unicorn Program Series

This program equips participants with proven strategies, cutting-edge research, and the best-in-class advice to fuel innovation, seize emerging tech developments, and catalyse transformation within your organization.

LocationUC Berkeley

Date02 - 07 Nov, 2025

LanguageEnglish

Asia Start: AI + Digital China Expedition

Asia Start provides entrepreneurs and executives with unparalleled access to Asia’s dynamic digital economy and its business ecosystems, offering the latest trends and insights, strategies, and connections to overcome challenges and unlock future growth for your business in Asia and beyond.

LocationShanghai, Hangzhou, Guangzhou, Shenzhen

Date17 - 21 Nov, 2025

LanguageEnglish

Smart Cities, Fintech, and Alternative Energy for the Global Future

In partnership with Columbia Engineering

Global Unicorn Program Series

This program is a transformative initiative designed to empower civil leaders and businesses in smart city development, fintech, alternative energy, and new energy sectors.

LocationDubai, UAE

Date15 - 19 Dec, 2025

LanguageEnglish

Opportunities in the Disruption of Traditional Industries

In partnership with The University of Sydney

Global Unicorn Program Series

The Global Unicorn Program in Disruption of Traditional Industries – presented jointly by CKGSB and University of Sydney – will emphasize Australia’s distinctive contributions.

LocationSydney, Australia

Date24 - 27 Feb, 2026

LanguageEnglish

AI-Driven Healthcare Innovation Program

In partnership with Johns Hopkins Carey Business School

Global Unicorn Program Series

The 2025 Artificial Intelligence (AI)-Driven Healthcare Innovation Program stands at the forefront of addressing the critical need for innovative healthcare solutions powered by artificial intelligence.

LocationJohns Hopkins University, Washington, D.C.

DateSummer 2026