Shanghai Stock Exchange: Baffling Bourse

March 16, 2015

Is the Shanghai Stock Exchange finally becoming a hub for global finance?

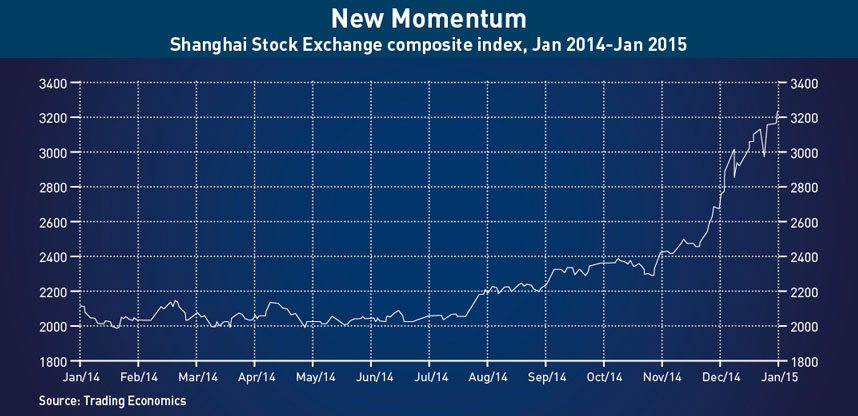

After a mainland equity collapse in 2007, investors the world over largely wrote off Shanghai’s stock exchange as the lesser cousin of regional heavyweight Hong Kong. But tides have turned thanks to the Hong Kong-Shanghai Stock Connect, which allows traders at each exchange to buy and sell certain stocks in the other. After said market linkup debuted, the Shanghai Composite Index rocketed upward from around 2,500 points to break the 3,000-point mark in less than a month, even as interest in the Stock Connect faltered. The sudden surge set foreign investors salivating once more at the prospect of snapping up Shanghai stocks.

As local retail investors and equities experts abroad turn their gaze upward to track Shanghai’s ascent, it is unclear whether most understand the financial foundations and regulatory system that underpin the workings of China’s foremost native stock exchange. Nor is everyone confident its gains tally with reality.

“People are still far more trusting of the US stock market as a leading indicator of the economy,” says Robert Blohm, a professor at China’s Central University of Finance and Economics. Blohm, while noting positive developments in earnings at Shanghai’s exchange, says that its erratic movements are similar to those of Tokyo’s in the late 1980s.

“The problem with the Japanese stock market at the time was that it was irrational; it wasn’t analysis-based,” Blohm says.

To understand how Shanghai’s exchange might move past that stage and overcome both a lack and overabundance of regulation requires a look back at its origins and often tumultuous development. How the Shanghai Stock Exchange became what it is today and how it is viewed both on and off the mainland by regulators and investors speaks volumes about where it is headed, and why.

Humble Beginnings

Shanghai’s stock market is a key component of China’s economic framework, as it was intended to be when it launched alongside the Shenzhen exchange in late 1990. Its debut marked the beginning of a suite of capitalist mechanisms that would be rolled out over the course of the following decade. As major companies from the mainland were formed out of smaller regional government enterprises and began listing in Hong Kong with so-called H-share offerings, that city’s exchange ballooned in size and importance to global finance. With experience gained there and in New York, mainland companies could then return to China to build the foundation of the country’s current state-owned enterprise (SOE)-dominated model.

Unfortunately market conditions stagnated following the Asian Financial Crisis of 1998, and from 2001 to 2005 the Shanghai exchange muddled its way through a four-year slump until a series of big deals and protection from stock dilution due to a temporary ban on IPOs turned things around. By the end of 2006 the Shanghai index had leapt from 1,000 points to 3,000 points in the space of just 18 months—only to go bust after reaching a historic peak of over 6,000 points in October of 2007. The plunge ended with the index finishing 2008 down a staggering 65%.

A partial recovery fueled by the government pumping cash into the country’s economy was not enough to rouse investor interest, and the composite index continued a chronic slump that, until this year, seemed doomed to continue. But it didn’t.

Surging Stocks

The broader trend upward this year, as tracked by the Shanghai Composite Index, entered the foothills of its current rally in mid to late July after the announcement of the Hong Kong-Shanghai Stock Connect. The index has continued upward ever since, outside a dip in December that it later recovered from. State media certainly encouraged investor optimism, as China Securities Regulatory Commission President Xiao Gang told the Xinhua-sponsored China Securities Journal the Stock Connect would speed Shanghai on its way toward becoming an international hub.

The latest leap, in which the bourse went from around 2,500 to over 3,000 points in the space of about a month, began in mid-November, just before the launch proper of the stock market linkup. But as the rally drove on it became clear that the Stock Connect was not as user-friendly as many international investors would have liked, says Haohao Zhou, China economist for ANZ.

“There’s just more counterparty risk involved than people had expected. It’s a nominee structure,” says Zhou, which means that the Hong Kong exchange acts as a clearing house. “If you want to sell your stock on a particular day you have to deliver all your stocks to the brokerage company before the trading kicks off. So you have more counterparty risk and most of the typical institutional investors in Hong Kong just do not feel comfortable enough with that.”

Nor do regulatory hurdles end at China’s borders, as many mutual funds out of Europe learned in November. Many were forced to hold off on participating due to their Luxembourg-based regulator having not yet given approval. But this is not the first instance of Europe playing catch-up with China’s opening capital markets: when the first RMB-denominated scheme for foreign investment on the Shanghai exchange began in 2011, it took authorities in Luxembourg roughly a year to grant approval for any investment funds to begin buying mainland stocks.

The current surge is also unusual in that previously the A-share market—regular shares that are also available to foreigners—mirrored China’s economy at large, growing and shrinking in tandem with broader macroeconomic trends. The key driver of the current uptick, in addition to attempts to profit off arbitrage between Hong Kong and Shanghai dual-listed stock valuations and an interest rate cut from the People’s Bank of China, is likely the protracted slump in real estate throughout much of China.

For now, the downturn appears to have effectively ended the property sector’s role as a dependable earner for institutional investors and profitable storehouse for value among retail investors—individuals buying and selling shares for their own personal account—at least outside of top-tier cities such as Beijing and Shanghai. That has left only one sector where profit is possible: equities.

Who’s Driving this Thing?

Although the Shanghai exchange is often decried as a casino, the latest influx of willing investors shows that such concerns are not enough to scare off everyone, and without real estate to spread out the risk, investment has no other destination as attractive as the stock market. That many retail investors view Shanghai as being driven by speculation and liquidity does not change the fact that depositing money with traditional banks requires enduring low interest rates, or that the bond market is still not worth the effort.

Shares in the CSI 300 index, compiled by the China Securities Index company, quoted below RMB 5 at the end of September had jumped 63% by mid-January, according to one Bloomberg report, suggesting that much of the rally has been driven by inexperienced retail investors whose knowledge of trading began with “buy low” and ended with “sell high”.

An auditor at a top Western accountancy firm, who declined to be named, says he’d been investing in mainland markets since his college days, and had snapped up securities firm shares in December on speculation that companies in the sector would cash in on the rally that month, in addition to SPD Bank stock he figured was undervalued. His stocks also included Ping’an—up nearly RMB 20 from his buying price of RMB 60 per share.

Meanwhile, a fellow auditor at the same firm, who also declined to be named, had got involved in the market too, but was still new to equities and couldn’t recall what he’d bought most of his stocks for. But he’d taken a beating from buying securities shares: like his colleague, he’d bought them in order to profit off the December rally, but his gains didn’t last long as some securities firms slumped by as much as 30%. He was still holding onto the shares when he spoke to CKGSB Knowledge, but at a growing loss.

Barriers Remain

Shanghai has entered global stock market indices, in a limited capacity, through the S&P China BMI, which measures all investible Chinese stocks available to global investors. After ups and downs from 2008-2011, the S&P has trended net positive to date, at least broadly speaking.

Shanghai has entered global stock market indices, in a limited capacity, through the S&P China BMI, which measures all investible Chinese stocks available to global investors. After ups and downs from 2008-2011, the S&P has trended net positive to date, at least broadly speaking.

But the Stock Connect that kickstarted the current boom remains only partially opened to international capital, limiting foreign investment to 568 designated stocks out of the total 971 listed in Shanghai. Furthermore, there is the process of first going through a broker in Hong Kong. Those barriers are likely to come down in time, but they point to a more central problem.

“Shanghai can’t really become an international finance center until they’ve opened up the capital account and made the renminbi fairly convertible on that capital account,” says Julian Evans-Pritchard, China Economist at Capital Economics. “In order to be an international financial center you need to be able to freely shift funds across the border and convert them into different currencies.”

There is certainly a desire to invest, as much of the international exposure to mainland shares now seems to be coming from privately traded derivatives in Hong Kong. A recent Reuters report found that thanks to regulatory and technical hurdles to foreign investment in mainland firms outside of an approved list, most Stock Connect activity was occurring off-exchange as funds bought “synthetic” equity—financial tools that grant exposure to a stock’s gains and losses—to increase their China exposure—this despite Beijing’s hopes that the new program would curtail said footloose foreign funds’ growth.

Zennon Kapron, founder and Managing Director of the China-based financial consulting firm Kapronasia, suggests that this focus on synthetic equity was likely to dissipate in the longer term as the market linkup’s scope broadened and regulations were eased. He adds that China’s lack of domestic derivatives was another factor that detracted from the Shanghai Stock Exchange’s international appeal, even as its impact on the global financial system increased.

“There are certainly a subset of these investors that have not come into the [Shanghai] market because of the inability to hedge,” Kapron says. “As we have seen in the latter half of 2014 and beginning of 2015, the Shanghai Stock Exchange can be quite volatile. Investors may not want to take a position in something that they cannot hedge, or they might not even be allowed to, based on investment rules.”

Furthermore, in comparison to exchanges like those in London and New York, tight-fisted regulation has kept Shanghai’s exchange comparatively undiversified. It generally favors heavyweight, state-owned firms, while smaller enterprises truly in need of willing global capital often get shunted to Shenzhen, which lacks a Connect of its own. Worse still, the abovementioned capital controls effectively rule out any international firms that might otherwise consider listing in Shanghai.

Still, domestic brokers’ eagerness to invest abroad could serve China well in finally opening up with Shanghai at the vanguard, says Robert Blohm, from the Central University of Finance and Economics. That outward-facing mentality contrasts with Japan, where a preference of investing in local firms has kept the stock market in Tokyo from becoming more of an international listings destination.

“If anything there’s an opposite propensity of Chinese to invest in foreign things,” says Blohm. “Shanghai has a lot more potential for internationalization than the Tokyo exchange ever had.”

Trust Issues

Global investor attention may have shifted to Shanghai’s side of the Stock Connect, but Hong Kong has something that Shanghai truly lacks: a sense of trust and security. “I think the bigger issue is trust and faith in the legal system,” Evans-Pritchard says. “It’s harder to build that trust, and I think there’s still quite a significant amount of wariness of how well investors’ rights will be protected in the mainland. Investors want exposure to China but they don’t necessarily want to deal with the legal uncertainties that would be involved in investing from within China itself.”

But even after a drop-off in participation from both sides of the new market linkup, all of the economists contacted viewed the Stock Connect as a step in the right direction toward opening up China’s capital account in a way that would benefit the international standing of the Shanghai Stock Exchange. It’s also set to get better as the suite of regulations is revised and the investment process for international investors is smoothed out, says ANZ’s Zhou. “The version that we currently have is not the final version,” he notes.

Stock Connect notwithstanding, in light of the bourse’s history and the latest trends in investment, it appears that while the Shanghai Stock Exchange may be of global interest, its offshore influence remains hobbled. Cumbersome controls that prevent global capital from flowing where it is most needed, and a murky regulatory environment keeps potentially willing international investors—or even international listings—off the table. The recent rally may have captured the world’s attention, but its speed and contrast with wider macroeconomic conditions again raise questions of its credibility.

This all may change in the long run as reforms are gradually rolled out. But so long as Shanghai’s market lacks the global liquidity and institutional trust that underpins other major stock exchanges’ financial fundamentals, its international significance will remain limited.

Enjoying what you’re reading?

Article Subscribe (1)

CKGSB Report

Related Articles

Our Programs

Asia Start: AI + Digital China Expedition

Asia Start provides entrepreneurs and executives with unparalleled access to Asia’s dynamic digital economy and its business ecosystems, offering the latest trends and insights, strategies, and connections to overcome challenges and unlock future growth for your business in Asia and beyond.

LocationChina (Shanghai, Hangzhou, Shenzhen)

Date11 - 14 May, 2026

LanguageEnglish

Scaling Innovation: AI and Digital Strategies for Business Transformation

Global Unicorn Program Series

In partnership with Columbia Engineering

This program is designed to equip senior executives with the strategic insights and tools necessary to lead in this transformative era.

LocationNew York, USA

Date27 Sep - 02 Oct, 2026

LanguageEnglish

Emerging Tech Management Week: Silicon Valley

Global Unicorn Program Series

In partnership with UC Berkeley College of Engineering

This program equips participants with proven strategies, cutting-edge research, and the best-in-class advice to fuel innovation, seize emerging tech developments, and catalyse transformation within your organization.

LocationUC Berkeley

Date01 - 06 Nov, 2026

LanguageEnglish

Stanford & Silicon Valley Immersion Program

Global Unicorn Program Series

In partnership with Stanford Engineering Center for Global & Online Education

This CKGSB program equips entrepreneurs, intrapreneurs and key stakeholders with the tools, insights, and skills necessary to lead a new generation of unicorn companies.

LocationStanford University Campus,

California, United States

Date06 - 11 Dec, 2026

LanguageEnglish with Chinese Translation