Aiming for the Top: Can China Escape the Middle Income Trap?

May 23, 2019

Since 1960, only 15 countries have escaped the so-called “middle-income trap.” Can China beat the odds?

At a meeting of world leaders near Beijing in November 2014, Chinese President Xi Jinping gave a speech that referenced an obscure theory of economic development. “This year we have…discussed ways of leaping over the middle-income trap,” he told the audience, which included US and Russian Presidents Barack Obama and Vladimir Putin, as well as Japanese Prime Minister Shinzo Abe.Hours later, on the same day, Xi brought it up again over dinner with the other heads of state. “Major new topics such as leaping over the middle-income trap … have been added to our agenda,” he told them.

First coined by two World Bank experts in 2007, the middle-income trap phenomenon—the existence of which is disputed by some economists—describes how growth in developing countries tends to stagnate when gross national income (GNI) per capitarises above a certain level, as higher wages push up production costs. Countries can become “stuck in the middle” as they struggle to compete with low-income newcomers where labor costs are still low, and advanced high-income economies with strong innovation.

The World Bank’s latest designation for high-income status is GNI per capita of at least $12,056. Brazil, who went through a period of spectacular growth before experiencing economic stagnation and eventual contraction, seems to have fallen into the middle-income trap, where its per capita GNI has leveled off at around $10,000,. The Philippines, the first country in Southeast Asia to begin industrializing in the early 1950s, has languished as a lower middle-income economy for more than half a century. In Mexico, GNI per capita has fluctuated in a narrow band between $8,000 and 9,700 for the past 25 years.

“Middle-income countries are not doing nearly as well under globalized markets as either richer or poorer countries,” says Linda Glawe, a researcher at Germany’s FernUniversität in Hagenand coauthor of a recent paper about China and the middle-income trap.

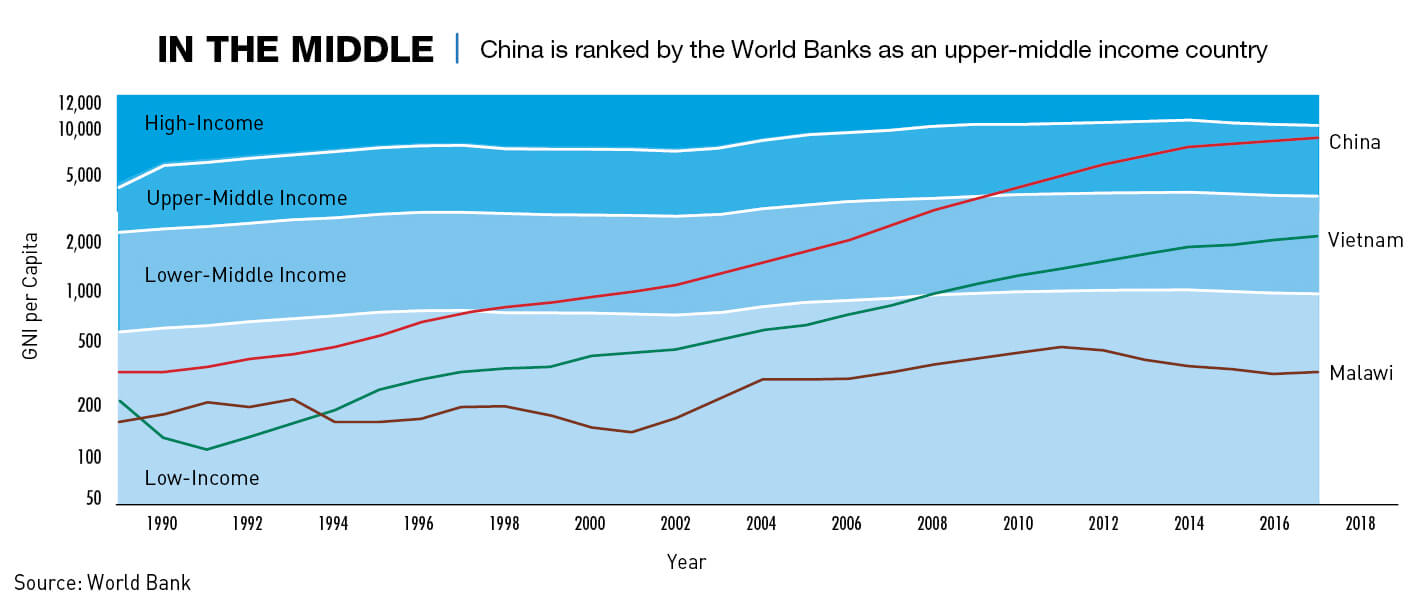

In recent years the middle-income trap has been increasingly discussed in the context of China, which used to make up much of the world’s poor, but now accounts for a growing chunk of its middle class. Since initiating market reforms in 1978, China has averaged GDP growth of nearly 10% per year—the fastest sustained expansion by any major economy in history—and lifted hundreds of millions of people out of poverty. Chinatoday accounts for the world’s second-largest share of global GDP after the United States, and in 2017 had a per capita GNI of $7,310—putting it squarely within the World Bank’s bracket for an upper middle-income economy.

The question is whether or not that is as good as it is going to get, as there is a view that China’s climb up the ladder of prosperity could be stalling. Instead of continuing to rise to high-income status, the country is in danger of becoming the biggest, most high-profile victim of the middle-income trap.

“In the long run, it’s hard to say. The possibility that China can get out of the middle-income trap in the short term or next 10-20 years is there, but relatively low,” says Yikai Wang, assistant professor at the University of Oslo’s Department of Economics.

In Beijing, China’s top leaders are said to be relatively upbeat about avoiding the potential “trap” and believe they have bigger issues to address, according to Wang Yong, deputy director of the Center of New Structural Economics at Peking University. “They are quite optimistic about moving out of the middle-income trap. Things are different after the global financial crisis occurred, when China’s leadership was really worried. But now, although China’s growth rate has slowed down, I think the top leadership has more ambitious goals than just avoiding the trap.”

Making the Leap

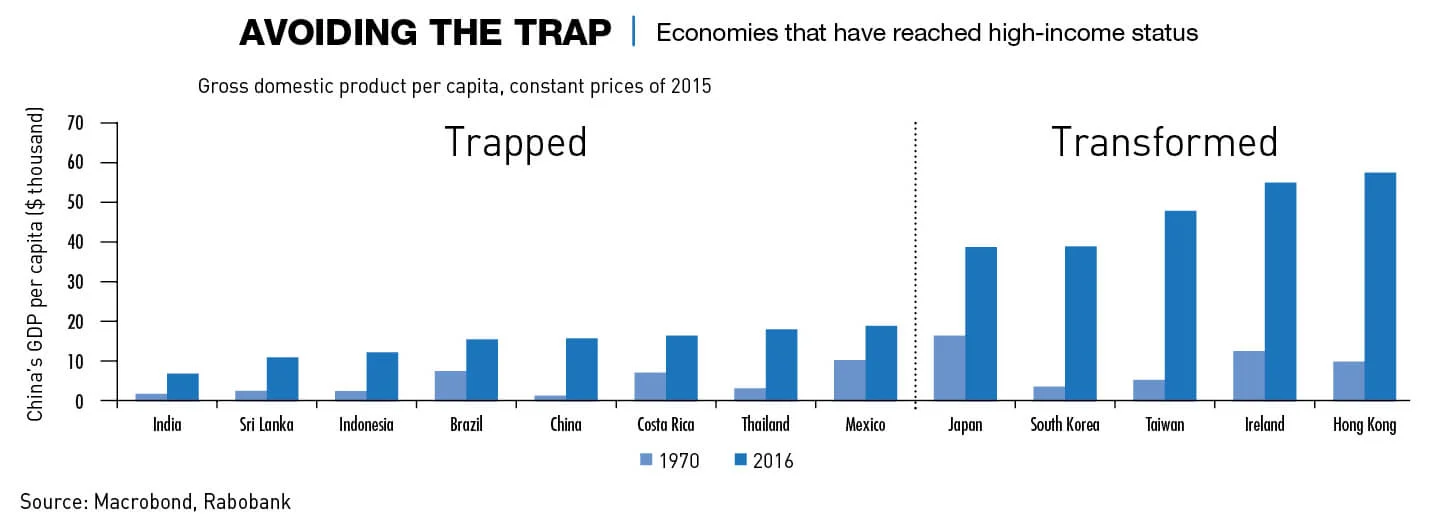

Although many countries in recent decades have emerged from poverty to enter the middle-income category, very few have made the additional leap to high-income status. In 2012, the World Bank found that only 15 out of 101 middle-incomeeconomies in 1960 had achieved developed status by 2010. Five were from East Asia—Hong Kong, Singapore, Japan, South Korea and Taiwan. And while escaping the middle-income category is difficult, it is also not impossible, with countries like Panama, Argentina and Croatia rising to join the ranks of high-income countries in 2018.

While many of these growth stories, particularly those in East Asia, offer relevant lessons for the Chinese mainland, China’s growth story is unique. It underwent rapid economic expansion from a low base starting in 1978. In the year that China’s late paramount leader Deng Xiaopinglaunched the reforms that kick started growth, it was very poor with a per capita GDP just 1.5% of the US. The low starting point and the size of China’s population were key factors in making the growth spurt unprecedented in its length.

Since then, in many ways China has followed a similar development path and growth trajectory to its northeast Asian neighbors, but it is not guaranteed to repeat the transformation they achieved. “If you compare China to these East Asian success stories, when they were at a similar development stage as China was in 2010, there are mixed results,” says Glawe. She points to three factors that will determine China’s ability to avoid the middle-income trap: human capital, export structure, and productivity.

Investment in human capital is critical, as there is a strong correlation between quality education and economic performance—a quality education system can stimulate creativity and in turn fuel innovation. But despite a huge cultural premium placed on academic achievement in China, human capital and education are areas where the country surprisingly trails its successful Asian rivals.

While less than one-tenth of China’s population had completed secondary educationin 1980, this reached a peak of 27.5% in 2000. In the following decade, however, the share declined, to 26.9% in 2005 and 22.9% in 2010—leaving China, by this measure, behind various Latin American and East Asian middle-income countries.

China fares better in export mix and productivity, the two other factors considered vital for overcoming the middle-income trap. Researchers consider the structure of a country’s exports—including export diversification and product quality upgrading—as an important trigger to escape the middle-income trap, as specializing in certain, more sophisticated products over others can generate higher growth rates.

“China’s export sophistication level is higher than what would be expected of its economic development,” says Glawe. “However, I think in the future, it’s important to have a stronger focus on the export upgrading instead of further diversifying the Chinese export basket.”

China remains fundamentally a poor country, with per capita GDP and GNI still very small compared to developed economies. But this also means there is plenty of room for growth in productivity, according to Wang. “Unless China experiences some kind of chaos, war, or something dramatic, I am confident economic growth will be quite steady. It will not be as high as before, but 4-5% is still very feasible for the foreseeable future. I think the government is also quite determined to achieve that,” he says.

Made in China

Chinese leaders have realized the need to nurture new methods of maintaining economic momentum, as the investment and exports that the economy has relied heavily upon in the past decade are beginning to reach their limits. The country has picked all the low-hanging fruit for advancing its technology, such as simple transfers of technology from importing machinery, and the initial phases of economic reform by marketization. To reach a high-income status, the country will have to cultivate new growth sources associated with innovation and technological progress, and accelerate industrial restructuring instead.

China has made some strides here, although it continues to lag behind more developed economies. Its expenditure on research and development (R&D)represented less than 1% of its GDP in 2000, but by 2016 it had more than doubled to 2.11%. While this was a notable improvement, China still trailed the likes of South Korea (4.24%), the US (2.74%), and Japan (3.15%).

China has fared better in the number of international patent applications filed—another common barometer of innovation—with 48,900 filed in 2017, second only to the US and nearly double the 25,544 filed in 2014. Of the top 10 global patent applicants in 2017, three were Chinese—Huawei, ZTE and display panel maker BOE Technology.

In recent years, the government has also stepped up its industrial restructuring efforts. Beijing’s bold high-tech industrial development push, dubbed “Made in China 2025”, aims topromote so-called ‘intensive manufacturing’ and fundamentally transform China’s manufacturing sector from being a global giant in volume and output, to a leading manufacturing power in quality and tech prowess.

This will be a departure from its growth experience over the past 40 years, which Wang says has been largely reliant on imitation. He highlights that doubts still remain over China’s ability to innovate. “China’s really good at reverse engineering, copy and paste. Imitation will become more and more challenging for China. So how can China switch from the previous investment-based growth mode to this innovation-based growth mode? It requires a fundamental change in China’s institutions and the whole system.”

As Beijing gropes for a new growth model, it needs to contend with demographic headwinds from an aging population. China’s working-age population has edged down since peaking in 2011and the United Nations has forecastthis decline toaccelerate in coming decades. This demographic change will act as a drag on both overall economic growth and the pace of per capita GNI gains, as it pushes down the labour force participation rate. There are signs this is already happening, as China’s employed population shrank year-on-year in 2018 for the first time on record—something that only happened in China’s neighbors after they had already reached high income levels.

“China already has a very old population relative to its current state of economic development,” says Glawe. “Compared with India, China is the complete opposite. India will profit a lot from their demographic dividend, but this is one of the opportunities that will not apply to China any more and could put additional pressure on China regarding the middle-income trap.”

While China’s leadership has acknowledged the existence of the middle-income trap, in some ways the current trajectory of policymaking is viewed by researchers as being more likely to hinder rather than help efforts to reach high-income status.

Nearly all countries that transitioned to high-income levels underwent liberalization as they became richer. Economic liberalization was also a key driver behind China’s rapid growth from the 1980s to the 2000s, but has largely stalled during the past decade.

More recently, the government has appeared to be intent on retaining control over large swaths of the economy. “State intervention is already harming productivity and is likely to be a growing constraint. It becomes harder for state planners to allocate resources effectively as a country gets richer,” says Chang Liu, China economist at Capital Economics.

Reforms have made progress in some areas, the most obvious being the opening-up of China’s financial sector. But in some other crucial areas, things appear to have moved backwards, according to Liu. “It is no coincidence that a few commodity-rich economies aside, the countries that successfully reached high income status all relied on the free market to allocate resources to a degree that China seems reluctant to embrace,” says Liu.

Decisions at the top

The jury is still out on whether Beijing will succeed in lifting China out of the middle-income trap, but domestic policy officials and experts have expressed confidence that it can. In April 2018, Justin Lin, the World Bank’s former Chief Economist, said that China was on track to ascend to high-income status by 2025. Wang has a similarly optimistic view, predicting that China would enter the World Bank’s high-income bracket of $12,000 no later than 2025-2027. “I’m quite confident China will exceed that threshold value, so it will escape the middle-income trap,” he says.

Other experts are more conservative in their outlook, citing structural headwinds that look set to become an increasing drag on China’s growth. “Over the next two decades, we expect China’s per capita GDP to increase by 70%—far less than the fivefold increase over the past 20 years,” says Liu. “Given that the US economy is likely to perform relatively well over this period, China will remain much poorer than the US in 20 years. That said, it would probably just reach high-income status by the World Bank’s standards.”

“I would think it’s going to take a very long time. It’s hard to guess, but I would think [by] 2050. I think there are a lot of problems that China needs to solve first, so it will be more difficult than what Japan or Korea went through,” says Yikai Wang from the University of Oslo.

With this year’s GDP growth target revised down again to 6.0-6.5%, Beijing has acknowledged that China’s stellar run of economic outperformance is becoming increasingly difficult to sustain. Slowing growth is now firmly established as China’s new normal. This presents a problem as robust growth needs to be maintained if China is to continue gaining ground on developed economies and move towards high-income status as an economy.

On Beijing’s current trajectory, and barring a major shift in the reform agenda, a combination of weaker investment, population aging and continued state intervention, it looks possible that China could stall in the middle-income area, which could have significant implications.

“If China… fails to catch up with the speed of integration in the global economy, the consequences will be severe, both for China and the global economy, says Yikai Wang. “If China’s trade and integration with the global market fails to keep improving and catching up with the needs of the technology and production changes in the global economy, then China will not be able to provide the manufacturing goods and services as it is doing now. Output and innovations in other countries and companies may not be able to grow as they are doing now.”

Enjoying what you’re reading?

Article Subscribe (1)

CKGSB Report

Related Articles

Our Programs

Scaling Innovation: AI and Digital Strategies for Business Transformation

Global Unicorn Program Series

In partnership with Columbia Engineering

This program is designed to equip senior executives with the strategic insights and tools necessary to lead in this transformative era.

LocationNew York, USA

Date27 Sep - 02 Oct, 2026

LanguageEnglish

Emerging Tech Management Week: Silicon Valley

Global Unicorn Program Series

In partnership with UC Berkeley College of Engineering

This program equips participants with proven strategies, cutting-edge research, and the best-in-class advice to fuel innovation, seize emerging tech developments, and catalyse transformation within your organization.

LocationUC Berkeley

Date01 - 06 Nov, 2026

LanguageEnglish

Asia Start (15th Edition): AI + Digital China Expedition

Asia Start provides entrepreneurs and executives with unparalleled access to Asia’s dynamic digital economy and its business ecosystems, offering the latest trends and insights, strategies, and connections to overcome challenges and unlock future growth for your business in Asia and beyond.

LocationChina (Beijing, Shanghai, Hangzhou & optional Shenzhen)

DateNovember 2-7, 2026

LanguageEnglish

Intelligent China: AI, EVs & Advanced Manufacturing

Participants may join the full 12-day journey or select individual modules based on their interests and priorities.

LocationBeijing, Shanghai & Hangzhou

Date12 Days

LanguageEnglish

Stanford & Silicon Valley Immersion Program

Global Unicorn Program Series

In partnership with Stanford Engineering Center for Global & Online Education

This CKGSB program equips entrepreneurs, intrapreneurs and key stakeholders with the tools, insights, and skills necessary to lead a new generation of unicorn companies.

LocationStanford University Campus,

California, United States

Date06 - 11 Dec, 2026

LanguageEnglish with Chinese Translation