Introduction

E-finance, loosely defined as the use of internet in the provision of financial services, has been a hot theme in the backdrop of China’s rapid development. From online brokerage services and e-commerce to credit management and online payments, many academics and industry professionals believe that the financial services industry as a whole is undergoing a fundamental transformation as a result of this phenomenon. To learn more about the rise of e-finance in China and globally, CKGSB collaborated with KPMG to hold its second breakfast seminar with senior executives of Japanese companies in Beijing on May 28th, 2014. Shedding light on the implications of e-finance were two distinguished speakers, CKGSB Associate Dean and Professor of Finance, Chen Long, and KPMG Partner, Raymond Cheong. The highlights of their insights are summarized below.

Guest Speaker #1 – Dr. Chen Long (Professor of Finance, Associate Dean of Alumni Affairs) Overview of E-finance in China: Money market funds, mobile payments and other trends

Alibaba as a case study?

To understand the drivers of China’s e-finance market, one can simply look at Alibaba as a relevant case study. Alibaba, China’s largest online commerce company, will likely go public later this summer, with a projected valuation anywhere from $135 to $250 billion. Although currently private and primarily focused on the Chinese market, the Company’s trading volume has already surpassed that of Amazon and eBay combined. So what is the story of Alibaba’s explosive growth that turned a RMB 100,000 investment by Jack Ma in 1999 to a Company valued in the hundreds of billions today? This story can be explained by three keywords: e-commerce, e-finance and big data.

After Alibaba successfully established its two primary trading platforms, Taobao (C2C) and Tmall (B2C), it became a popular choice for China’s increasingly consumer-driven market. However, at that time, trading volume, sales and popularity still lagged behind the existing leader in Chinese C2C, Yi Qu. So how did Alibaba overtake the market in such a short amount of time? It did so by establishing a link between online commerce and online payment, creating a vertically integrated business that offered accessibility, convenience and security to the millions of online shoppers in China. Alibaba noticed that commerce created an increased demand for finance, and thus created an integrated ‘payment and settlement’ model to complement its e-commerce platform.

The establishment of Zhi Fu Bao, Yu’E Bao and micro loans tremendously enhanced Alibaba’s popularity and user base. It was especially successful in China because the existing financial system was underdeveloped, with a lack of investment and credit tools and well as numerous interest rate restrictions for banks. Therefore, these payment and investment vehicles served to fill this demand gap, helping Alibaba take advantage of the weakness of Chinese banks and capitalize on the opportunity.

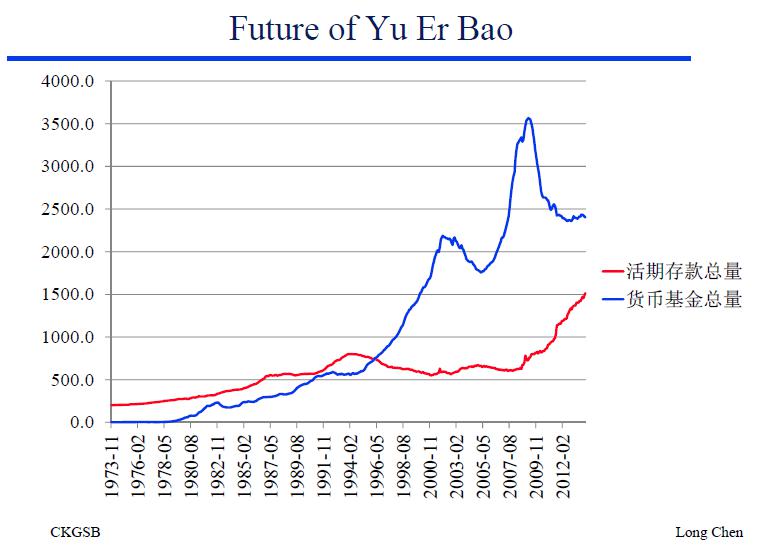

As Yu’E Bao is not classified as a bank and therefore is not subject to reserve requirements and other banking regulations, it was able to offer substantially higher interest rates to its investors. At the same time, money market funds such as Yu’E Bao can only invest in short-term loans from the highest-rated institutions, minimizing risk. As can be seen from the graph below, this helped money market fund deposits to quickly outgrow traditional checking account deposits in China over the past 10 years, a trend that is projected to continue over the coming years, especially with the introduction of internet finance. In the U.S. for example, money market deposits are currently four times higher than checking account deposits.

What’s next for e-finance?

It’s apparent that Alibaba has been a first mover by combining payment with commerce, with Google, Amazon and Apple trying to follow suite to develop comparable payment services. So what’s next for the e-finance industry? As the internet increasingly shifts from PC to mobile, there will be a rapid migration and emphasis on mobile payments, and Companies who are best positioned for this transition to mobile will reap the benefits of this transformation. Mobile payments will be especially critical in the O2O (“online-to-offline”) world, where it will effectively link the real world with the online world and serve as a source of information flow, capital flow and logistic flow. This is already evidenced by certain O2O businesses such as Didi Taxi, who has integrated mobile payment into its model.

While the age of e-finance is China is certainly upon us, we are definitely poised for continuous growth and innovation, much of which will fundamentally alter China’s financial system. Baidu, Alibaba and Tencent (“BAT”) were the first wave of innovative businesses to leverage e-finance, and will certainly serve as examples and role models for the next waves to come.

Guest Speaker #2 – Raymond Cheong (Partner, KPMG) Mobile Payments in China: Disruptive in Actions

What is the current state of mobile payments?

The acceleration of smartphone adoption has resulted in an eruption of the mobile payment market, especially in China. For example, 55% of China’s internet users have made a mobile payment, versus only 19% of U.S. internet users. The transactional value of global mobile payments has skyrocketed from only $240 billion in 2011 to nearly $1 trillion forecasted by 2015. Additionally, the shift from PC to mobile is more and more apparent, with smartphones being the most common starting place for online activities (versus PC only a few years ago).

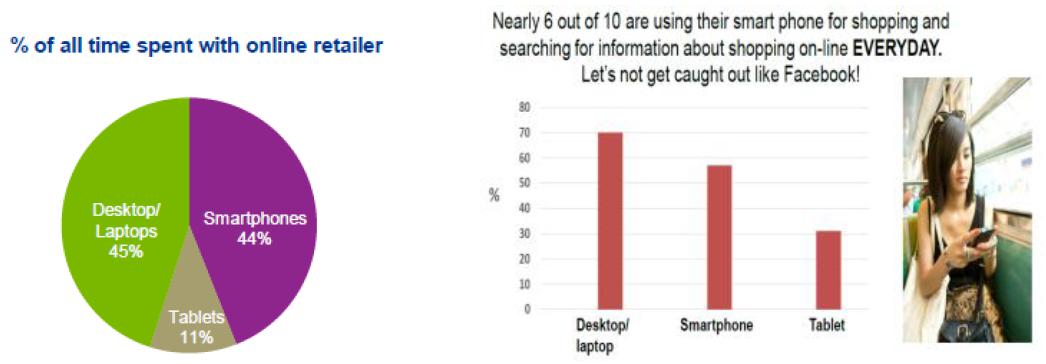

Driven by exponential growth in user base, China is embracing the technologies related to mobile payments and is making use of all the latest technologies. This trend is evidenced by the top consumer mobile applications survey completed in 2012, with money transfer applications holding the #1 spot (followed by location-based services and mobile search). Consumers now spend more time interacting with online retailers on smartphones and tablets than they do on desktops and laptops.

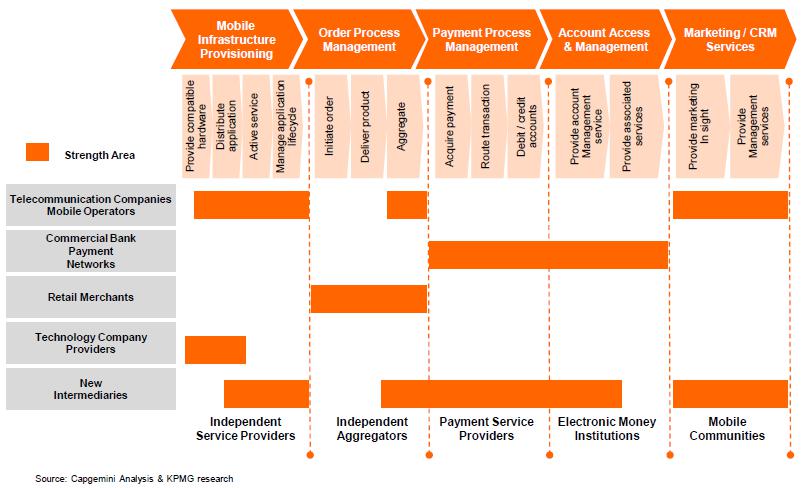

Who are the mobile players in the mobile payments value chain?

Interestingly enough, it’s the internet and technology companies that will lead the mobile payments market share over the next two to four years, not banks. Within China’s C2B payment industry, growth will be contributed by China’s e-commerce market. With respect to B2B, Alibaba currently dominates this market with over 79 million registered users and a marketplace with importers and exporters from over 240 countries and regions. The B2B market currently accounts for approximately 85% of gross merchandise value in China’s e-commerce market.

Where are the trends for mobile payments?

There are three primary trends for mobile payments: O2O, enforced security, and partnerships with banks.

O2O has become very prevalent in the mobile world, including making purchases through mobile apps, QR code scanning for commercial purposes and deal-of-the-day websites such as Groupon, Gilt Group and Living Social. The effect will be an increased degree of digitalization in the retail market, which will ultimately help the growth of location-oriented businesses. There are various benefits of O2O. First, it will allow businesses to track every transaction that is done and monitor the effects of campaigns in each channel. Second, O2O will benefit from the diversity of online advertising methods, while providing customers with the real-life experience with products offline. Last but not least, it will help businesses track and study consumer behavior by pushing advertisements on a real-time basis.

Despite the countless security measures that have been implemented through e-commerce transaction phases, e-commerce providers are still facing various security threats give the nature of the industry. As the mobile payments industry matures, we will see increase self-imposed security measures and regulatory requirements governing the industry.

Lastly, we will begin to witness the application of value-added services such as mobile wallet and microfinance within mobile payments. For example, China Merchants Bank began cooperating with Tencent’s WeChat in May 2013 to provide social media banking. What began as a basic service that notified customers about things like their account balances and credit card purchases has expanded to an offering range of banking services, including money transferring and credit card payment.

How will mobile payments transform your business?

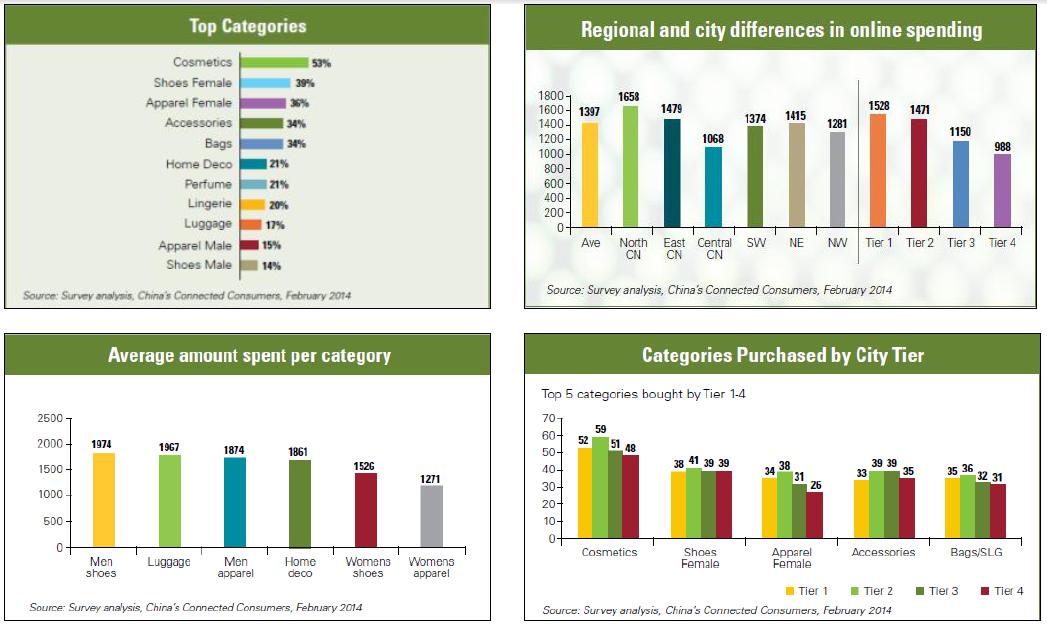

So what impact will the rise of mobile payments have on your business? There are a variety of factors that will impact this effect, such as retail category, geographic presence, price range, and the targeted demographic population. For example, the top three categories for online spending, based on a survey by “China’s Connected Consumers”, are cosmetics, female shoes and female apparel. From a geographic perspective, Northern China holds the title for greatest amount of mobile spending, while Central China has the least. Males tend to spend more than females when purchasing online, and 45-49 is the age group with the highest expenditures.

As e-commerce has become the single largest drive of total retail sales in China (representing over 20% of total annual retail sales growth), there will be increased scrutiny on promoting and regulating its growth so as to ensure a sustainable and secure path forward.

References

Powerpoint slides by Professor Chen Long – ‘E-finance in China: Money market fund, mobile payment, and other trends’

Powerpoint slides by Raymond Cheong – ‘Mobile Payments in China’*

* These presentation slides and associated comments from Raymond Cheong, which have been prepared for the breakfast meeting, are based on specific facts and circumstances in China. They should not be relied upon by any other person. Those who choose to rely on these slides and/or comments do so at their own risk. To the fullest extent permitted by law, KPMG in China accepts no responsibility or liability to them in connection with the slides and / or comments.